Epigamia: Building India's First Premium Dairy Snacking Category

- 2 days ago

- 12 min read

Executive Summary

Between 2015 and 2024, Drums Food International's brand Epigamia accomplished something that large dairy cooperatives and multinational FMCG companies had not: it created, named, and came to define an entirely new premium snacking category in Indian dairy — Greek yogurt. Starting with a pivot from a seasonal preium ice cream brand (Hokey Pokey), Epigamia built India's first branded Greek yogurt product and, by FY24, had scaled to ₹180 crore in annual revenue across 25,000+ retail touchpoints in 30+ cities, with investment from Verlinvest, Danone Manifesto Ventures, and Bollywood actor Deepika Padukone. This case examines the brand-building architecture, positioning logic, channel strategy, and the strategic pivots that enabled Epigamia to operate as a category creator rather than a category challenger.

Industry & Competitive Context

India's dairy market is paradoxically large and undifferentiated. While India is the world's largest milk producer, the organized value-added dairy segment — premium yogurts, flavored milks, probiotic drinks — remained structurally underdeveloped well into the 2010s. The market was dominated by cooperatives (Amul, Mother Dairy) and regional players competing primarily on price and volume, with virtually no innovation in premium functional formats. When Epigamia launched in June 2015, the Greek yogurt segment in India was, by all commercial accounts, non-existent as an organized category. While Danone had made limited attempts to introduce Greek-style yogurt in India before 2015, no brand had invested in category education, distribution infrastructure, or consumer communication at scale. The traditional curd (dahi) dominated the household consumption of fermented dairy, priced at mass-market levels. This structural gap — between a nutrition-aware urban consumer base and an absence of premium, functional dairy innovation — defined the white space that Epigamia entered. The competitive dynamics were asymmetric: Epigamia faced no direct branded competition in Greek yogurt, but had to overcome the formidable presence of deeply embedded dahi consumption habits. The competitive threat was not from rival Greek yogurt brands, but from the consumer's own existing product routine.

Brand Situation Prior to Launch

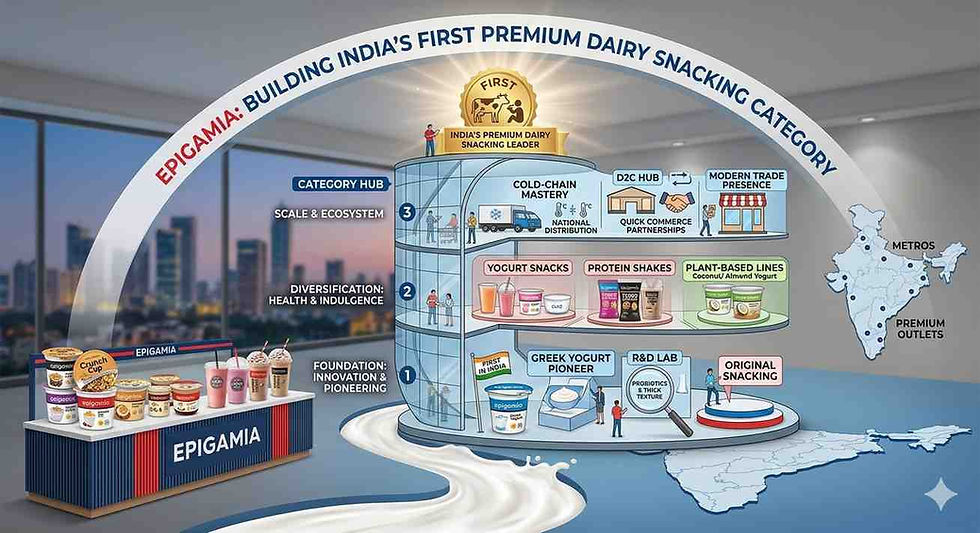

Drums Food International, the parent company, was founded in 2008 by Rohan Mirchandani (Wharton MBA), Ganesh Krishnamoorthy, and Milap Shah, initially launching Hokey Pokey — a premium artisanal ice cream brand with live kitchen stores. Hokey Pokey gained recognition as a category innovator in premium ice cream, but the business faced structural limitations: ice cream is a seasonal product with peak summer demand, requiring high store rents year-round, significant front-end staff, and a frozen supply chain requiring capital-intensive infrastructure. The critical insight that triggered the pivot was operational rather than purely strategic: managing a frozen supply chain (for ice cream) and a cold chain (for yogurt) simultaneously with limited resources was not viable. Greek yogurt, by contrast, has a 15-day shelf life from manufacturing to consumption — a logistical challenge, but also a powerful quality signal. As documented in Booming Brands (Harsh Pamnani, Westland Books, an account sourced from the founders' public narrative), the team explicitly chose "to give up the good to go for the great," discontinuing active focus on Hokey Pokey to concentrate on Epigamia. The brand name itself carried strategic intent: in ancient Greek, "Epigamia" referred to a peace treaty formalizing the dynastic relationship between Alexander the Great's successor Seleucus and India's Chandragupta Maurya — a cultural bridge between Greece and India, which the founders used as a metaphor for bringing Greek yogurt tradition to the Indian market.

Strategic Objective

Epigamia's founding strategic objective was not market share capture within an existing category — it was category creation. The brand sought to establish Greek yogurt as a distinct, desirable snacking format in the minds of urban Indian consumers, specifically differentiating it from traditional dahi on three axes: protein content (approximately 2x that of regular curd), absence of preservatives or artificial ingredients, and versatility of consumption occasion. The brand's stated positioning, as articulated by Rohan Mirchandani in multiple public forums including an Indian Retailer-published talk series ("Brick by Brick: Building Insurgent Brands" with DSG Consumer Partners), was to create a "fresh FMCG brand offering snacking solutions with natural functionality." The aspiration was to contemporize India's traditional dairy industry, not merely add a new SKU to existing shelves.

A secondary but equally important objective was building a sustainable, fundamentally sound business — a priority that the founder explicitly acknowledged had been temporarily displaced by growth-at-all-costs mentality during early funding rounds, and later recorrected. In a 2023 interview with Just Food, Mirchandani stated: "We took a conscious call late last year that we're going to focus on building a fundamentally sound business." This strategic correction — prioritizing unit economics and profitability over top-line velocity — proved formative for the brand's medium-term trajectory.

Positioning & Consumer Insight

Epigamia's positioning rested on a precise consumer segmentation choice, publicly described by Mirchandani in the Indian Retailer-published talk series. The target cohort was defined as health-conscious, SEC A and B consumers, aged 25–30, college-educated, with gainful employment and purchasing power for premium products. Crucially, the team also targeted individuals who were in a relationship or newly married — a life-stage choice premised on the insight that this cohort was transitioning from individual consumption decisions to joint household purchasing decisions, and was therefore receptive to upgrading food choices as part of identity signaling. The positioning was built on the concept of "no compromise" — that a consumer need not choose between health and taste. This anti-trade-off narrative was central to all consumer-facing communication and directly addressed the primary psychological barrier to trial: the assumption that healthier products inherently sacrifice flavor. Critically, Epigamia chose not to position itself as a dairy product — it positioned itself as a snack. This single framing decision had compound consequences for occasion mapping, channel selection, and communication strategy. As documented by Mirchandani's public comments, approximately 33% of consumers used Epigamia as a breakfast option, 33% as an inter-meal snack, and 33% as a post-dinner dessert — a tri-occasion utility that the "snack" positioning enabled, where a "dairy product" framing would have confined it to a narrower usage context. The brand also faced a specific consumer education challenge: Greek yogurt was widely perceived as an expensive, foreign version of dahi with no meaningful differentiation. Overcoming this required not advertising, but education — a deliberate strategy of "teach before you sell," executed through in-store sampling, infographic packaging (clearly communicating high protein, low fat, no preservatives), and social content explaining concepts like live cultures and gut health in accessible language.

Brand Architecture & Product Strategy

Epigamia launched with Greek yogurt as its hero product and expanded its portfolio through a principle of strategic product adjacency — each extension sharing either the same ingredient base, the same target consumer, or the same consumption occasion as the core product. The documented product trajectory moved from Greek yogurt to artisanal curd, smoothies, mishti doi, snack packs, lactose-free variants, plant-based coconut milk yogurts, and eventually high-protein "turbo shakes" and milkshakes. As reported by Mirchandani in a 2024 interview (via News On Projects), the high-protein product line — launched approximately eight months prior — was already contributing 12% of total company revenue, targeting what the CEO described as a consumer base of approximately 95–100 million protein-aware consumers in India. This figure was stated publicly as a demand-side sizing, not an internal metric. The plant-based range (coconut milk yogurts) was launched via Epigamia's D2C platform and positioned as India's first in the segment — an innovation claim the brand has made publicly through press channels. The portfolio logic, across all extensions, maintained a consistent brand promise: better-for-you, fresh, preservative-free, with functional nutrition. The brand's naming choice — Epigamia, carrying deep cultural and historical resonance — provided a distinctive semantic foundation that elevated it above generic "healthy yogurt" labeling, supporting a premium price architecture without requiring constant justification.

Channel Strategy & Distribution Architecture

Epigamia's distribution strategy evolved in three distinct phases, each corresponding to a funding and market-development stage.

Phase 1 (2015–2017): Credibility-first, premium modern trade. The brand entered through high-trust premium retail environments — Foodhall, Godrej Nature's Basket, Reliance Fresh, and similar modern trade chains. This was not simply a logistical choice; it was a positioning decision. Being stocked alongside imported and premium food products established perception of quality and aspirational value before mass reach. Simultaneously, the brand partnered with fitness centers, yoga studios, and gyms, and participated in events such as the IIT Bombay Mumbai Marathon 2017 — directly accessing health-conscious consumers in contextually relevant settings, as documented by the brand's agency Rasta in their published work portfolio.

Phase 2 (2018–2022): Distribution scale and multi-channel expansion. As documented through multiple news sources, Epigamia scaled from approximately 4,000 to 10,000 to over 25,000 retail touchpoints, expanding across 30+ cities. This included entry into kirana (general trade) stores, which required purpose-built cold chain logistics — a supply chain capability the brand built internally and which won the Global Logistics Excellence Award from the Tata Strategic Management Group for Supply Chain Excellence in Dairy Products. The 15-day shelf life constraint, which could have been a bottleneck, became a competitive moat: it forced operational excellence that larger, ambient-product competitors did not develop.

Phase 3 (2022–2024): Digital and quick commerce dominance. As confirmed by Mirchandani in a 2023 Just Food interview, digital channels (D2C, e-commerce platforms, and quick commerce) collectively contributed 33% of Epigamia's revenue, with quick commerce described as the "fastest-growing" digital segment. By 2024, quick commerce (platforms such as Blinkit, Swiggy Instamart, Zepto) accounted for approximately 47–48% of total revenue, as stated by Mirchandani in a 2024 interview published by News On Projects. This shift is strategically significant: quick commerce delivery of a 15-day shelf-life perishable product at 8–30 minute delivery windows is structurally aligned — the cold chain requirement that limited traditional distribution became an advantage in quick commerce, where refrigerated dark-store infrastructure was already in place.

Celebrity Equity Architecture: The Deepika Padukone 7. Partnership

In May 2019, Drums Food International announced a multi-crore strategic partnership with Bollywood actor Deepika Padukone, as reported by Business Standard, YourStory, and Inc42. The investment was made through KA Enterprises LLP, Padukone's strategic investment vehicle, and was part of an extension of the Series C funding round led by Verlinvest and including Danone Manifesto Ventures and DSG Consumer Partners.

The partnership was structured not as a conventional endorsement deal but as a combined investment-plus-advisory-plus-ambassador arrangement. Padukone took equity in Drums Food International and simultaneously became the brand's face and a strategic advisor, with a stated focus on advising on product launches, consumer feedback, and expansion into new cities. As Mirchandani stated at the time: "Her involvement will accelerate the pace of reach for our products." The strategic logic was audience alignment: Padukone's publicly documented health-conscious lifestyle and her positioning as an aspirational yet relatable figure for urban Indian women aged 20–35 directly mirrored Epigamia's core target segment. The equity stake, as reported by YourStory via Ministry of Corporate Affairs filings, involved the allotment of 5,833 equity shares at a face value of ₹100 with a premium of ₹1,705.50 per share — valuing the company at approximately $68.52 million at that point.

The arrangement represents a structurally evolved model of celebrity-brand partnership: rather than a transactional spokesperson contract, it created aligned incentives (financial upside for the celebrity in brand success), increased credibility of endorsement, and positioned the partnership as a genuine brand story rather than a media buy.

Investor Architecture & Strategic Partnerships

Epigamia's funding history reflects a carefully curated investor architecture, not simply capital accumulation. The Series A in 2016 was led by DSG Consumer Partners and Verlinvest, a Belgium-based consumer-focused investment firm. Danone Manifesto Ventures — the venture fund of global dairy leader Danone — subsequently invested, providing both capital and category validation: the world's largest dairy-focused consumer company bet on Epigamia's category thesis. As of 2024, Verlinvest remains the largest shareholder with approximately 30% stake, as reported by Inc42 citing a Moneycontrol report. Total disclosed funding across rounds reached $81.2 million per Tracxn data. The investor mix — a consumer-focused PE (Verlinvest), a strategic dairy player (Danone), a venture fund (DSG Consumer), and a celebrity entrepreneur (Padukone) — collectively provided distribution credibility, sector validation, media visibility, and operational capital. In FY23, Epigamia's sales crossed ₹168 crore (₹135.7 crore in FY22, a 24% increase), as reported by Inc42 citing regulatory filings. Total revenue including other income reached ₹172 crore. FY24 revenue was reported at ₹180 crore by Tracxn. Net loss in FY23 was ₹67 crore, up from ₹59.5 crore in FY22 — reflecting the investment phase of the business. However, the company achieved its first EBITDA-positive April in 2023, and as Mirchandani confirmed to Just Food, reached FY23 total revenue equivalent to approximately $24 million (then approximately ₹196 crore). The company was reported to be near EBITDA positive on an annual basis by FY24.

Business & Brand Outcomes

The following outcomes are derived from verified public sources:

Revenue trajectory: From an estimated $15 million (~₹110 crore) in FY20 (as stated by Mirchandani in a 2020 Just Food interview) to ₹168 crore in FY23 and ₹180 crore in FY24 (Tracxn data), representing consistent multi-year growth in a structurally challenging perishable FMCG category.

Distribution scale: Growth from approximately 4,000 retail touchpoints at Series C to 25,000+ touchpoints across 30+ cities by 2024, as stated publicly by the company.

Quick commerce revenue share: Quick commerce channels grew from the "fastest-growing digital segment" (2023, Mirchandani, Just Food) to approximately 47–48% of total company revenue by late 2024 (Mirchandani, News On Projects, October 2024).

Product portfolio: Expanded from the original Greek yogurt launch to 20+ SKUs across Greek yogurt, artisanal curd, smoothies, snack packs, mishti doi, plant-based yogurts, and high-protein product lines within approximately nine years.

Category creation: No verified third-party market share data for the Greek yogurt segment has been publicly disclosed. However, Epigamia is widely referenced as the category creator and category leader in organized Greek yogurt in India by credible trade and business publications. Specific market share percentages cited in the public domain are not independently verified and are therefore excluded from this analysis.

Valuation: As of December 2023, Epigamia's valuation was reported at approximately ₹1,250 crore (~$150 million) by multiple business publications citing market sources.

No verified public information is available on CAC, LTV, gross margin percentages by SKU, or specific brand equity measurement scores.

Strategic Implications

Category creation as the highest-leverage brand strategy. Epigamia's central strategic lesson is that in markets with low category penetration, the primary competitive task is consumer education, not competitor conquest. The brand invested early in sampling, nutritional communication, and occasion creation — all of which built a category before building a market share. This is structurally distinct from how late entrants (Amul, Mother Dairy introducing their own Greek-style variants) would need to compete: as challengers in a category defined by Epigamia's attributes.

Cold chain as a strategic moat, not a cost center. Epigamia's 15-day shelf life constraint forced the development of cold chain logistics capability that most FMCG players in India had not built. Rather than treating this as a margin drag, the brand converted it into a quality signal and a logistics award — and, as quick commerce infrastructure proliferated, this capability became directly monetizable as a channel advantage. The lesson for premium food brands is that supply chain constraints, if resolved with excellence, can become barriers to imitation.

The investor-as-ecosystem strategy. Danone's participation was not merely financial — it validated the category thesis for modern trade buyers, distributors, and potential hires. Verlinvest's consumer brand expertise and Padukone's audience alignment collectively created a brand ecosystem that no single capital provider could. For founders building challenger brands in conservative categories, the investor selection decision is a brand decision.

The profitability pivot and its timing implications. Epigamia's deliberate shift from top-line growth to profitability in late 2022 — including a 75% reduction in marketing spend and a one-third reduction in distribution footprint — reflects a strategic maturation that many D2C-era brands failed to execute. The willingness to shrink distribution to 25,000 stores from a higher level in order to improve unit economics is a textbook application of portfolio rationalization, and it restored operational profitability (at the EBITDA level) before the brand re-accelerated growth.

Quick commerce as a structural advantage for cold-chain FMCG. Epigamia's ascent to ~47–48% quick commerce revenue share by late 2024 is not accidental — it reflects a structural alignment between the platform model (refrigerated dark stores, 10–30 minute delivery) and the product model (preservative-free, 15-day shelf life, requires refrigeration). As quick commerce expands into Tier 2 and Tier 3 cities, brands with cold-chain-native products are disproportionately advantaged. This represents an important GTM implication for health-food and functional FMCG brands considering entry strategies.

Discussion Questions

Category Creation vs. Market Share Competition: Epigamia chose to create the Greek yogurt category rather than compete within existing dairy segments. Using frameworks such as Blue Ocean Strategy and Byron Sharp's "Mental Availability," evaluate whether Epigamia's category creation approach is replicable for other premium food brands entering underpenetrated Indian markets. What are the conditions under which this approach fails?

The Celebrity Equity Model: Epigamia's partnership with Deepika Padukone combined investment, endorsement, and advisory roles rather than a conventional media contract. Assess the strategic advantages and risks of this combined celebrity-equity structure compared to traditional endorsement agreements. Under what brand and market conditions does the equity model add more strategic value than the contract model?

The Profitability Pivot: In 2022–23, Epigamia deliberately reduced marketing spend by 75% and cut distribution to improve unit economics, achieving EBITDA breakeven in April 2023. Critically evaluate this decision using the Ansoff Matrix and lifecycle theory. Was the timing optimal? What risks did this rationalization create for brand equity and competitive positioning?

Cold Chain as a Strategic Moat: Epigamia built cold chain logistics as a core internal capability — not outsourced — and won a national logistics award for it. Evaluate whether this was the right vertical integration decision for an early-stage FMCG brand. Use the VRIO framework to assess whether cold chain capability constitutes a sustainable competitive advantage for Epigamia in an era where quick commerce platforms are investing in their own refrigerated infrastructure.

Scaling Beyond Premium: Epigamia's documented expansion plans target Tier 2 and Tier 3 cities and smaller, more accessible SKUs. Analyze the strategic tension between maintaining premium brand positioning and pursuing mass distribution. Drawing on analogies from global FMCG brands (e.g., Chobani in the US, Danone globally), what brand architecture and pricing decisions should Epigamia consider as it moves down-market without diluting its core equity?

Comments