OYO's Revenue-Sharing Model with Hotel Partners: From Aggregator to Franchise and the Road to Profitability

- Mar 26

- 11 min read

Industry & Competitive Context

India's budget and mid-market hospitality sector is structurally among the most fragmented in the world. As of the early 2010s, when OYO entered the market, the segment was characterised by thousands of unbranded, sub-scale properties operating with poor occupancy, inconsistent service standards, and no access to centralised distribution infrastructure. Travellers faced unpredictable experiences; hotel owners operated with limited technology, poor pricing discipline, and negligible marketing reach. This structural gap — between an underserved consumer demand and an under-equipped supply side — was the founding opportunity that OYO identified and pursued.

The competitive landscape against which OYO's model must be evaluated includes two distinct categories of competitor: traditional online travel agencies (OTAs) such as MakeMyTrip, Goibibo, and Booking.com, which offer hotel owners distribution access without operational involvement; and branded budget hotel chains such as Ginger Hotels and Treebo, which attempt to standardise the budget segment through tighter but less scalable franchising models. OTAs typically charge commissions in the range of 15–20% of the gross booking value without imposing brand standards or operational involvement. OYO's proposition was structurally differentiated from both: it offered hotel owners something that neither OTAs nor traditional chains could — branded identity, centralised demand aggregation, and technology-led operational tools — at the cost of pricing control and a commission premium.

The Indian hospitality sector's organised and branded segment, according to a joint report by Hotelivate and other industry trackers, closed 2023 with decade-high occupancy of 66.1%, an average daily rate of ₹6,869, and rising revenue-per-available-room metrics. This macro tailwind provided the demand environment within which OYO's model was tested, stressed, reformed, and ultimately validated.

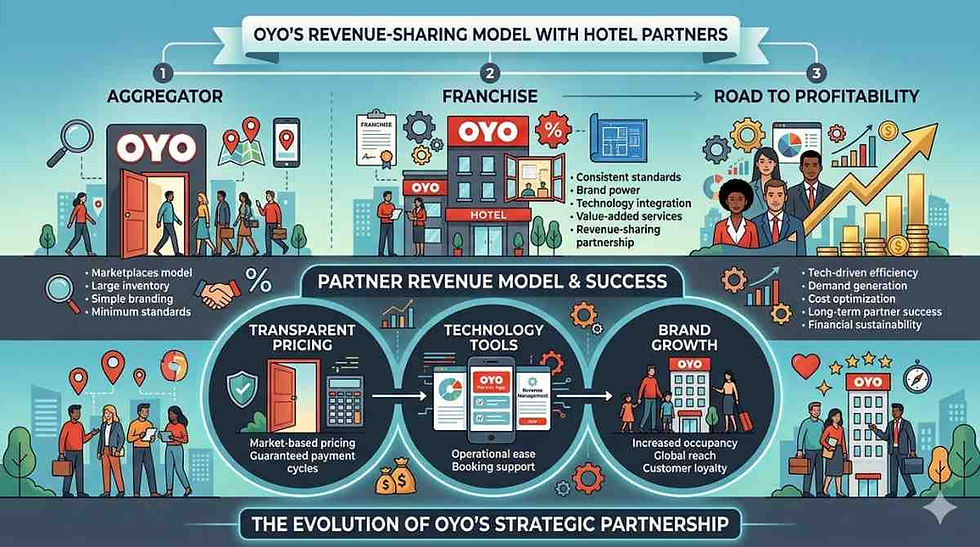

Brand Situation Prior to the Strategic Pivot

OYO was founded in 2013 by Ritesh Agarwal as Oravel Stays, with the company launching as OYO Rooms in May 2013. In its earliest iteration, the business operated as a pure aggregator — OYO leased a subset of rooms from partner hotels, standardised and rebranded them, and offered them to consumers through its platform at a take-up rate. Hotels provided the physical inventory; OYO provided the branding, booking technology, and guaranteed occupancy for the leased portion.

This model solved an immediate problem for both sides. For hotel owners, OYO offered guaranteed revenue on leased rooms regardless of occupancy — a proposition that was commercially attractive in a market where independent hotels frequently experienced severe occupancy volatility. For consumers, OYO offered a consistent, predictable experience in a segment previously defined by unpredictability.

The aggregator model, however, carried structural weaknesses that became commercially unsustainable at scale. First, the minimum guarantee commitment created asymmetric financial risk for OYO — the company was obligated to pay hotel owners a fixed floor amount irrespective of actual demand, which generated significant cash burn during periods of low occupancy. Second, by controlling only a leased subset of rooms within each property, OYO had limited operational authority over the full guest experience. Third, as OYO's platform grew and hotels became increasingly dependent on OYO-generated demand, a power dynamic evolved that was commercially useful for OYO but created the conditions for future partner dissatisfaction.

In 2015, OYO began a deliberate transition from the aggregator model to a franchise model. As documented in press reporting and confirmed by the company's DRHP filed with SEBI in 2021, this shift accelerated through 2016 and was largely complete by the time the DRHP was filed. Under the franchise model, OYO no longer leased rooms or committed to minimum guarantees on a standard basis — instead, hotel partners operated under the OYO brand, used OYO's technology platform, and paid OYO a commission on gross booking value.

Strategic Objective

The overarching strategic objective behind OYO's shift to a revenue-sharing model was to decouple the company's financial performance from the fixed-cost obligations of the minimum guarantee structure, while retaining the supply-side scale and demand-side brand equity it had built through the aggregator phase.

From a business model perspective, the shift was a move from a fixed-cost, asset-heavy demand guarantee structure to a variable-revenue, asset-light commission structure. As documented in OYO's DRHP filed with SEBI in 2021, the company stated explicitly that following COVID-19, it had changed its business model to a revenue-sharing arrangement under which it takes a commission of 20–35% on gross booking value — net of discounts and loyalty points — from its hotel partners. The DRHP further confirmed that at its peak, 14.7% of hotels had minimum guarantee arrangements, a number that had been reduced to nearly zero by the time of filing.

From a marketing strategy perspective, the objective was equally significant: by standardising the OYO brand experience across a large inventory base and driving consumer demand to that inventory through centralised technology and pricing, OYO could build brand equity that attracted consumers irrespective of which underlying property they stayed in. In this model, consumer loyalty accrued to the OYO platform, not to individual partner hotels — a structural dynamic that both underpinned OYO's commercial moat and became the source of significant partner-level conflict.

Campaign Architecture & Execution

The execution of OYO's revenue-sharing model has three documented dimensions: technological architecture, commercial contracting, and brand standardisation. These are not marketing campaigns in the traditional sense, but they represent the strategic deployment of a business model that itself functions as a market development tool.

On the technology side, OYO developed a proprietary property management system — referred to publicly as OYO OS — that hotel partners used to manage bookings, check-ins, housekeeping, room pricing, and performance analytics. The platform also included a dynamic pricing engine that, according to publicly reported company descriptions, executed real-time price adjustments across its inventory to optimise revenue for both OYO and its partner hotels. This technology infrastructure was OYO's primary value proposition to hotel partners beyond brand access and distribution — it gave small, independently operated hotels access to yield management tools that would otherwise be inaccessible to them.

On the commercial contracting side, OYO introduced a self-onboarding tool called "OYO 360," documented in the company's DRHP, which allowed new hotel partners to digitally generate and sign contracts based on property details and KYC documents. The DRHP confirmed that in FY2021, almost all new hotel partner contracts were signed and managed digitally. This automation of the partner onboarding process was a structural enabler of rapid scale — it allowed OYO to add hotel partners at a pace that would have been impossible through manual contracting processes.

On brand standardisation, OYO enforced minimum quality benchmarks as a condition of partnership — clean bedding, reliable Wi-Fi, air conditioning, hygiene protocols — and required partner properties to display OYO branding externally. This standardisation was both a consumer-facing quality promise and a contractual mechanism for OYO to maintain control over the experience delivered under its brand.

Positioning & Consumer Insight

OYO's core consumer insight was straightforward and was validated by the scale of latent demand in the Indian budget travel segment: a substantial proportion of Indian travellers — domestic, business, and leisure — were not adequately served by either premium hotels they could not afford or unbranded budget properties they could not trust. The value proposition was not premium experience at a lower price; it was reliable, predictable experience at a budget price point.

The positioning strategy was built on two simultaneous audience commitments: to the end consumer, OYO positioned as quality-assured, consistently deliverable budget accommodation; to the hotel partner, it positioned as a demand-generation partner that could demonstrably improve occupancy. OYO's DRHP cited its own data showing that the median revenue for a storefront improved 1.9 times within 12 weeks of joining the OYO platform in India — and 2.4 times in its European vacation homes business.

The strategic sophistication of OYO's positioning lies in its two-sided market logic. Unlike traditional brands that build equity by communicating with consumers, OYO had to simultaneously build credibility with hotel partners — a B2B audience whose partnership decisions determined the supply-side availability of the product that consumers experienced. This dual positioning requirement is structurally analogous to the challenge faced by marketplace platforms such as Uber and Airbnb, but was complicated by the fact that OYO imposed far more operational and branding constraints on its supply side than either of those platforms did.

The Partner Conflict: A Documented Strategic Failure

No analysis of OYO's revenue-sharing model would be analytically complete without examining the documented failure of its minimum guarantee commitments — the episode that both necessitated the shift to pure revenue sharing and nearly destroyed the company's supply-side ecosystem.

As reported extensively by Economic Times, Inc42, The News Minute, and other credible outlets between 2019 and 2020, hotel partners across India began filing public complaints, organising protests, and approaching regulatory bodies over OYO's alleged failure to honour its minimum guarantee commitments. The Federation of Hotel and Restaurant Associations of India (FHRAI) filed a formal complaint with the Competition Commission of India (CCI) in July 2019, alleging that OYO had been levying undisclosed charges — including promotional fees, convenience fees, walk-in penalties, and audit charges — that effectively negated the minimum guarantee amounts promised to hotel owners.

A documented example of this dynamic: a hotel partner with a 20-room property might be promised a minimum guarantee of ₹4 lakh per month. From this, OYO deducted platform fees, GST, and various other charges, reducing the effective payout significantly below the contractually promised amount. Hotel partners also alleged that OYO controlled their online listings in ways that prevented them from taking direct bookings, concentrating consumer demand entirely through OYO's platform and creating a dependency that reduced partners' negotiating power.

The COVID-19 pandemic accelerated the rupture. As reported by MediaNama and Economic Times, in early 2020 OYO invoked force majeure clauses to suspend minimum guarantee payments to hotel partners, citing pandemic-driven demand collapse. FHRAI stated publicly that many hotel partners' original contracts did not contain force majeure provisions, characterising OYO's action as a unilateral contract breach. In parallel, OYO proposed replacing existing agreements with a new revenue-sharing structure. By this point, as reported by Business Standard, over 500 hotels in 100 cities had disassociated from OYO since April 2019 alone.

This episode is strategically instructive because it reveals the structural tension inherent in any two-sided platform that uses supply-side incentives to achieve rapid scale. The minimum guarantee was not irrational as a growth tactic — it solved the chicken-and-egg problem of onboarding hotel partners before OYO had proven consumer demand at scale. But it created financial obligations that OYO could not sustainably honour at the commission levels it was charging, and it was withdrawn in a manner that damaged trust with the very partners whose participation was essential to the model's viability.

Business & Brand Outcomes

The financial trajectory of OYO's business, as documented through its DRHP, annual reports, and credible press reporting, tells a story of extreme growth followed by a painful contraction and a documented return to profitability.

At the peak of its expansion phase in 2019, OYO's valuation reached $10 billion, as reported by multiple credible outlets. By 2020, as a result of the pandemic, partner conflicts, and cash burn from its minimum guarantee model, the valuation had declined to approximately $3 billion. By its June 2024 funding round — a down round as reported by Business Standard and Inc42 — the valuation stood at approximately $2.37 billion.

The commercial reset, however, generated measurable financial improvement. According to OYO's audited annual report for FY2024, as reported by Business Standard: the company posted a net profit after tax of ₹229 crore — its first-ever full-year profit. This was achieved despite a marginal decline in total revenue to ₹5,388.78 crore from ₹5,464 crore in FY23. The turnaround was driven primarily by a 16% reduction in total expenditure, with employee costs falling 52% to ₹744.3 crore. The company's adjusted EBITDA grew 215% to ₹877 crore in FY24 from ₹277 crore in FY23, representing eight consecutive quarters of positive adjusted EBITDA, as stated in the company's own communications.

Looking forward, founder Ritesh Agarwal communicated to employees — as reported by Inc42 citing PTI — that Q4 FY25 revenue was expected to reach ₹2,100 crore, representing 60% year-on-year growth. A significant contributor to this growth was the acquisition of G6 Hospitality — parent company of Motel 6 and Studio 6 in the US and Canada — from Blackstone Real Estate for $525 million, completed in September 2024. OYO's hotel inventory in India grew from 12,938 properties in FY23 to 18,103 in FY24, indicating that the reset of partner economics had not permanently damaged the platform's ability to attract new hotel partners.

OYO's parent company, PRISM, filed a confidential DRHP with SEBI in January 2026 — its third IPO attempt — targeting a raise of ₹6,650 crore at a valuation of $7–8 billion, as reported by Outlook Money and Moneycontrol. This represents a material recovery in perceived enterprise value from the $2.37 billion down-round valuation of mid-2024.

No verified public information is available on OYO's specific market share data by revenue or room-nights in the Indian budget hotel segment.

Strategic Implications

The OYO case generates four strategic implications of direct relevance to platform businesses, marketplace founders, and growth marketers in the Indian and global context.

The first implication concerns the incentive architecture of two-sided platform models. Minimum guarantees are structurally effective as a supply-side acquisition tool in the early phase of a marketplace, because they reduce the risk threshold for small suppliers considering platform participation. However, they create financial obligations that scale with supply inventory — not with demand revenue. OYO's experience demonstrates that when the gap between minimum guarantee commitments and actual demand-generation capacity widens at scale, the result is simultaneous cash burn for the platform and partner dissatisfaction that can trigger regulatory and reputational consequences. The strategic lesson is that early-stage supply incentives must be designed with an explicit off-ramp to performance-based structures before the incentive liability becomes a balance sheet liability.

The second implication concerns pricing power and dependency risk in franchised ecosystems. By centralising dynamic pricing control and directing consumer demand exclusively through its own platform, OYO created a structural dependency among hotel partners that was commercially useful but strategically dangerous. Partners who had surrendered pricing autonomy and direct customer relationships in exchange for guaranteed demand found themselves with no independent revenue base when OYO's minimum guarantees were suspended. The CCI complaints and mass hotel exits documented between 2019 and 2020 were not merely commercial disputes — they were the predictable consequence of an incentive architecture that prioritised platform control over partner sustainability.

The third implication concerns the relationship between operational scale, unit economics, and brand equity. OYO's expansion to over 150,000 properties across 35 countries — pursued while the minimum guarantee model was still in operation — generated global brand recognition but simultaneously degraded service quality and partner satisfaction. The decision, documented as part of OYO's turnaround strategy in FY23, to delist thousands of hotels in order to focus on quality over quantity represents an important strategic precedent: in branded hospitality, the value of supply-side scale is bounded by the brand equity implications of quality inconsistency. Adding inventory that damages guest experience destroys more brand equity than it generates in revenue.

The fourth implication concerns the role of technology as a value proposition in B2B partner models. OYO's proprietary hotel management system, dynamic pricing engine, and digital contracting platform were not incidental features — they were the structural basis on which the revenue-sharing model was commercially defensible. Hotel partners paid OYO 20–35% of gross booking value in exchange for something that OTAs could not offer at a comparable commission: operational infrastructure, brand access, and demand generation simultaneously. As OYO has matured toward profitability, the technology stack has become both its defensible moat against OTA competition and its primary value proposition to the next generation of hotel partners it needs to onboard.

MBA Discussion Questions

1. OYO's shift from a minimum guarantee model to a pure revenue-sharing arrangement was necessitated by both a financial crisis and a partner relationship breakdown. Using principal-agent theory, evaluate whether the minimum guarantee model was structurally misaligned from inception, or whether it was an appropriate early-stage incentive that was poorly managed at scale. What contractual design principles should two-sided platform businesses apply when structuring supply-side incentive models?

2. OYO's DRHP documented that median hotel revenue grew 1.9 times within 12 weeks of joining the platform. However, the same period also saw mass partner exits and CCI complaints. How do you reconcile these two data points? What does this paradox reveal about the difference between average platform value creation and the distribution of value extraction across different partner segments?

3. OYO operates in a market where its primary supply-side partners — independent hotel owners — are also its primary source of competitive differentiation. As OYO moves toward a public listing and targets institutional investors, evaluate the strategic tension between maximising commission rates to improve reported margins and maintaining partner economics that sustain supply-side growth. How should this tension be reflected in OYO's IPO-stage narrative?

4. The Federation of Hotel and Restaurant Associations of India (FHRAI) approached the Competition Commission of India against OYO, alleging predatory pricing and abuse of dominant position. Using Porter's Five Forces framework, assess whether OYO's control over online listings, pricing, and consumer demand constitutes a legitimate competitive advantage or a structural barrier that regulators are justified in scrutinising.

5. OYO's acquisition of G6 Hospitality in the US for $525 million marks a strategic shift from asset-light aggregation to owning branded hospitality IP in a new market. How does this acquisition alter OYO's business model risk profile, and what does it signal about the long-term limitations of the asset-light franchise approach in markets where branded hospitality infrastructure is already well-developed?

Comments