SUGAR Cosmetics: Building a Digital-First D2C Beauty Brand in India's Colour Cosmetics Market

- Apr 27

- 13 min read

Executive Summary

SUGAR Cosmetics represents one of the most analytically instructive cases of digital-first brand building in the Indian D2C ecosystem. Founded in 2015 by Vineeta Singh and Kaushik Mukherjee — both IIM Ahmedabad alumni — the brand emerged not from a venture capitalist's trend thesis but from three years of first-party consumer data accumulated through a prior business, FAB BAG. By the time SUGAR launched its first products, the founders had proprietary insight into what Indian millennial women were buying, what frustrated them about existing offerings, and what formulation gaps the market had left unaddressed. This case examines how that foundational consumer intelligence was translated into a coherent digital-first strategy, a disciplined content-over-performance-marketing philosophy, and a phased omnichannel expansion that has driven the brand to Rs 505 crore in revenue in FY24 — while pursuing a path toward IPO readiness.

Industry & Competitive Context

India's colour cosmetics market sits at an inflection point. Multiple industry research firms place it in the range of USD 3.4–4.8 billion in FY2024, with projected growth at a CAGR of approximately 7–8.5% through the early 2030s, driven by rising disposable incomes, urbanisation, digital media penetration, and a structurally younger population that has normalised everyday makeup use. Despite this scale, the category's structural dynamics at the time SUGAR entered were deeply unfavourable to new entrants. Two competitive tiers defined the market. At the mass end, Hindustan Unilever's Lakmé commanded shelf space and distribution depth built over decades, while Maybelline (L'Oréal Group) had established strong urban recall through aggressive mass media investment. At the premium end, MAC and Bobbi Brown — both Estée Lauder properties — served aspirational consumers through department stores and limited distribution. What the market conspicuously lacked was a credible mid-market proposition designed specifically for Indian skin tones, Indian climatic conditions, and an Indian millennial consumer who was increasingly making purchase decisions through digital content rather than television advertising. This gap was structural rather than incidental. Global brands formulate products primarily for Western skin tones and temperate climates. The transfer of product lines to India without reformulation meant that lipsticks faded, foundations oxidised, and eyeliners smudged in India's heat and humidity. Indian brands, constrained by legacy positioning and retail-first thinking, had not moved decisively to fill this space for younger, digitally-native consumers. The resulting white space — affordable, performance-oriented, India-first colour cosmetics marketed through digital channels — was the opening SUGAR's founders had identified through their FAB BAG experience.

Brand Situation Prior to Launch: The FAB BAG Advantage

Understanding SUGAR's strategy requires understanding its unusual pre-history. In 2012, Vineeta Singh and Kaushik Mukherjee launched FAB BAG, a monthly beauty subscription service that curated five products from global and emerging Indian brands for a subscriber base of primarily urban women aged 21 to 30. The service grew to approximately 200,000 customers over nine years and, by 2014, had achieved profitability at roughly $1 million in revenue. FAB BAG's strategic contribution to SUGAR's eventual launch was not financial but informational. Running a beauty subscription business for three years gave the founders real behavioural data on Indian women's beauty preferences: which product categories had highest repurchase intent, which formulation attributes (transfer-proof, long-lasting, matte finish) were most requested, and what shade ranges Indian consumers found chronically underrepresented. As Vineeta Singh described in an interview published by IndiaQuotient, analysis of FAB BAG subscriber data revealed a persistent consumer frustration with makeup that failed to survive India's heat, humidity, and long commutes — a functional failure that neither international brands nor domestic incumbents had adequately addressed. This research grounding — three years of direct-to-consumer behavioural data on SUGAR's eventual target audience — constitutes what strategists would recognise as a proprietary consumer insight asset. The founders were not entering colour cosmetics on assumption or trend observation; they were entering with specificity about what their customer needed and what the market was not providing. The pivot itself was capital-constrained. When the co-founders decided in 2015 to shift from subscription curation to original product manufacturing, their remaining capital was approximately Rs 25–30 lakh, a portion of which was reserved for subscriber refunds. Their first products — an eyeliner and a kohl pencil — were sourced from a manufacturer in Germany. They subsequently required Rs 1 crore from seed investor IndiaQuotient simply to import the first batch of lipsticks. The brand's initial scaling was therefore achieved under conditions of extreme capital efficiency, a constraint that shaped its early reliance on content and organic digital distribution over paid performance marketing.

Strategic Objective

SUGAR's founding strategic objective, as articulated by Vineeta Singh in multiple publicly documented interviews, was to build a performance-driven, India-first colour cosmetics brand for the millennial woman — one that combined international-grade formulation with deep understanding of Indian skin tones, Indian weather conditions, and the purchasing behaviour of a consumer who was increasingly digital-first but not yet fully e-commerce native. Two sub-objectives shaped execution. The first was category relevance: to establish SUGAR as the brand of choice specifically for long-lasting, transfer-proof, and weather-appropriate makeup at accessible price points — occupying a mid-premium "masstige" positioning between mass-market domestic brands and premium international ones. The second was distribution reach: recognising that approximately 85–95% of India's beauty and cosmetics market transacted offline, the founders articulated a clear long-term objective of building omnichannel distribution at scale. As Vineeta Singh stated publicly: "To give a good fight to the Unilevers and the L'Oreals, we had to build omnichannel distribution."

The tension between these objectives — a digital-first launch philosophy and an eventual offline-first revenue reality — defines the strategic architecture of SUGAR's growth and distinguishes it from both pure-play e-commerce brands and traditional beauty incumbents.

Campaign Architecture & Execution

Digital-Only Launch (2015–2017)

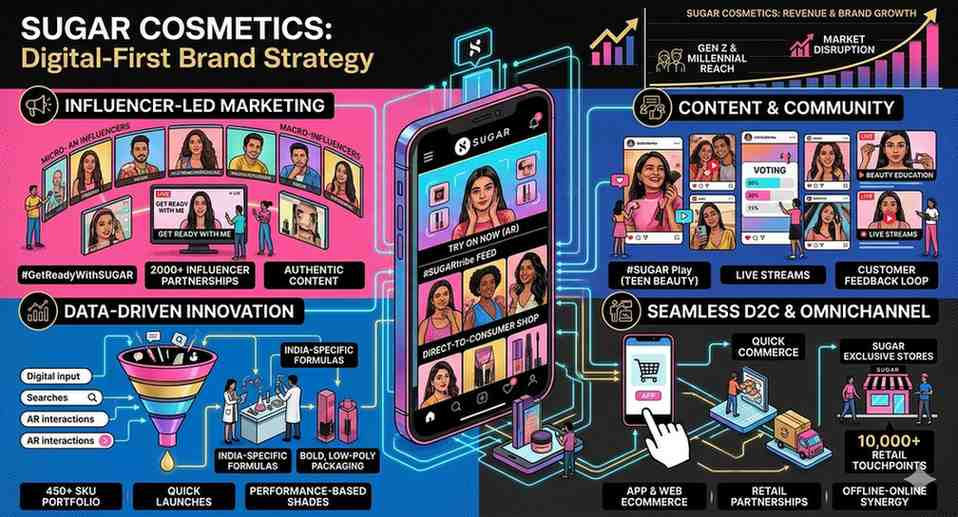

SUGAR launched exclusively on digital channels — its own website, and early marketplace listings — with a product range developed around the specific functional insight from FAB BAG data. Initial SKU count was deliberately small, focused on lip products (lipsticks, lip liners) and eye products (eyeliners, kajals) — categories with high visibility, high purchase frequency, and strong shade-range requirements. The brand's early marketing approach was markedly different from the performance-marketing playbooks adopted by most e-commerce startups of the period. Rather than prioritising paid acquisition, SUGAR invested in content marketing across Instagram and YouTube — creating tutorials, shade guides, and educational makeup content that established the brand as an authority voice rather than merely a transactional seller. As Vineeta Singh explained in an interview with YourStory: "The one thing that we did well was being obsessed with the idea of using content, digital and social media to reach the consumer, and to do it in a very capital-efficient way, instead of spending on influencers." The brand built an in-house content team — women with genuine makeup expertise — to produce this material, internalising what most brands outsource. This content-first orientation had strategic logic beyond capital efficiency. In colour cosmetics, the purchase decision is inherently educational — consumers need to understand how to apply a product, which shades suit which skin tones, and how to build a look. By becoming the content that informed those decisions, SUGAR built brand familiarity and product confidence simultaneously. It was building mental availability through the very content touchpoints where its target consumer was spending time.

Omnichannel Transition (2017 onwards)

Two years after launch, SUGAR formally shifted to an omnichannel strategy, beginning its entry into physical retail. This was not a reversal of digital conviction but a recognition of market structure: with roughly 85–95% of colour cosmetics revenue transacting offline, a digital-only brand would be permanently capacity-constrained. The offline expansion followed a tiered logic: first, exclusive brand outlets (EBOs) and kiosks in high-footfall mall environments; second, partnerships with large-format retail chains including Shoppers Stop and Lifestyle; and third, general trade distribution into smaller multi-brand beauty stores and pharmacy chains. The brand opened its 200th standalone store as a milestone, and has expanded to over 45,000 retail touchpoints across more than 550 cities, as confirmed by company press communications and logistics partnership announcements. Critically, SUGAR continued expanding its offline presence even during the COVID-19 pandemic, a period when many competitors were reducing physical retail footprints. This counter-cyclical investment — opening new brand retail stores during the pandemic, strengthening its content and digital presence simultaneously — positioned the brand well for the post-lockdown recovery period. As per publicly cited data, 65% of SUGAR's total revenues are now generated through offline channels, and 60% of overall business comes from markets outside Tier 1 cities.

App, Sub-Brands & Portfolio Expansion

In November 2019, SUGAR launched its proprietary mobile application, which crossed 1 million downloads within the first year. The app strengthened direct-to-consumer capabilities and data ownership, supplementing marketplace revenues with first-party transaction data. The brand also undertook portfolio architecture decisions: in January 2022, SUGAR acquired a 51% majority stake in ENN Beauty, a natural skin and hair care brand, signalling diversification into the adjacencies of skincare and hair care. The company launched sub-brands including SUGAR POP (more accessible price points) and SUGAR Play (teen cosmetics), extending reach across consumer segments without diluting the core SUGAR brand's masstige positioning.

Positioning & Consumer Insight

SUGAR's brand positioning can be analysed through two frameworks: functional and attitudinal. Functionally, the brand positioned its products around the three specific performance attributes Vineeta Singh has cited consistently in public interviews — long-lasting wear, transfer-proof formulation, and suitability for India's tropical climate. This was a rational product claim grounded in a real consumer frustration and technically differentiated at launch from what incumbents were offering. The matte lipstick and smudge-proof kajal categories became anchor products because they embodied this positioning most vividly.

Attitudinally, SUGAR positioned itself as the brand of the bold, independent, aspirational Indian millennial woman — one who wore makeup not for occasions or social compliance but as a daily expression of identity. The brand's visual identity — high-contrast black and neon packaging, confident brand voice, and shade names with attitudinal personality — was designed to signal this attitudinal distinction from the more conventional femininity projected by legacy domestic brands. This dual positioning — functionally rigorous and attitudinally distinct — allowed SUGAR to compete on product merit against incumbents while simultaneously building emotional resonance with a consumer segment that felt unrepresented by established brand codes. The PETA-certified cruelty-free positioning, established from launch, added a values layer that resonated with younger, conscious consumers without requiring pricing or formulation compromises. The consumer insight at the core of SUGAR's positioning is the Jobs To Be Done (JTBD) principle applied to daily use: Indian millennial women needed makeup that performed through a full working day in a tropical climate, delivered in shades relevant to Indian complexions, at price points that didn't require the brand to be a special occasion. No incumbent — domestic or international — had built a primary identity around solving this specific job at SUGAR's price point.

Media & Channel Strategy

SUGAR's media and channel strategy has been characterised by a deliberate de-emphasis on paid digital performance marketing in favour of owned and earned media — a philosophically distinct approach from most D2C brands of its generation. The primary owned media investment has been in-house content on Instagram and YouTube — tutorials, makeup education, shade comparisons, and trend-responsive content created by SUGAR's internal team. By Vineeta Singh's public account, SUGAR's in-house content reached approximately 250 million monthly engagements across marketing channels at the time of the YourStory interview (published March 2021). The brand has also described generating YouTube content with 800,000+ views as a long-term brand awareness investment rather than a direct sales driver — an attribution philosophy that prioritises brand building over short-cycle performance returns. The brand has also invested in out-of-home (OOH) advertising — large-format placements in malls and on strategic highway and city locations — reflecting the recognition that brand awareness needs to be built across multiple touchpoints as the brand scaled into offline retail markets. In July 2023, SUGAR entrusted the Mumbai-based agency OMP India with the comprehensive management of its media strategy — a formal acknowledgment of the brand's need for more sophisticated multi-channel media planning as it scaled. Strategic collaboration was used selectively for cultural relevance: in August 2023, coinciding with the second season of Amazon Prime's "Made in Heaven," SUGAR launched an exclusive co-branded "SUGAR x Made in Heaven" cosmetics kit, leveraging content-commerce alignment without the recurring cost of a celebrity endorsement retainer. In September 2022, actor Ranveer Singh became a "brand evangelist" with an undisclosed investment — a move that combined investor participation with influencer credibility in a single partnership. Distribution across online marketplaces (Nykaa, Amazon, Flipkart, Myntra) expanded the brand's addressable market while its own website and app maintained direct consumer relationships. The combination created a multi-channel online presence without dependence on any single platform.

Business & Brand Outcomes

The following data points are sourced from Registrar of Companies (RoC) filings as reported by credible financial publications, confirmed press releases, and public investor communications.

Revenue: SUGAR's revenue from operations reached Rs 505.10 crore in FY24, up 20% from Rs 420.28 crore in FY23. This followed a 90% year-on-year growth in FY23. The company's net revenue in FY20 was publicly cited at Rs 105 crore.

Profitability: Net loss narrowed by 11.3% to Rs 67.58 crore in FY24, from Rs 76.24 crore in FY23. Total expenses grew 15.5% to Rs 583.72 crore. Advertising and sales promotion represented the largest single cost centre at Rs 161.6 crore in FY24 — approximately 27% of total expenditure.

Distribution Scale: Over 45,000 retail touchpoints across 550+ cities, including 200+ exclusive brand outlets. The brand opened its first flagship store in New Delhi in 2022.

Digital Reach: The proprietary mobile app crossed 1 million downloads within its first year of launch (2019–2020). No verified post-FY21 app download data is publicly available.

Funding: SUGAR raised a $50 million Series D round in May 2022, led by L Catterton — the world's largest consumer-focused private equity firm — with participation from A91 Partners, Elevation Capital, and India Quotient, at a reported valuation of approximately $500 million. Total funding raised to date has been publicly cited at approximately $85–95 million across multiple rounds. A further fundraise was confirmed from Anicut Capital in November 2024 (Series E).

IPO Trajectory: As of January 2024, Vineeta Singh confirmed publicly to ET Now that the company was targeting an IPO within a two-to-three year timeline, subject to achieving Rs 1,000 crore or more in revenue and demonstrated profitability.

Valuation: Reported at approximately Rs 4,100 crore as of 2024, per media coverage citing investor and market data.

Market Position: SUGAR has been publicly described as India's third-largest colour cosmetics brand, as noted in a logistics partnership press release in 2024.

No verified public information is available on SUGAR's customer acquisition costs, customer lifetime values, specific channel-wise revenue breakdown by individual product SKU, or specific digital advertising return on investment metrics.

Strategic Implications

The Pre-Launch Consumer Intelligence Model: SUGAR's founding advantage was not capital, connections, or a proprietary technology — it was three years of direct behavioural data from FAB BAG's 200,000-strong subscriber base. This gave the founders an unusual clarity about product-market fit before a single SUGAR product was manufactured. The strategic implication is the value of adjacent businesses as structured market research — a model rarely available to founders who enter a category cold, but replicable in principle through community-building, subscription platforms, or beta programmes that generate real behavioural data.

Content-Over-Performance-Marketing as Brand Equity Investment: SUGAR's decision to invest in owned content rather than performance marketing was capital-driven initially, but has produced a durable structural advantage: a brand identity built through educational content establishes category authority that paid advertising cannot replicate. In colour cosmetics, where the purchase is inherently discovery-driven and tutorial-influenced, being the content layer that educates the consumer creates a deeper relationship than being the brand that interrupts them with an ad. This is consistent with the concept of "Mental Availability" — ensuring the brand comes to mind first in purchase-triggering situations — but achieves it through utility rather than repetition.

The Omnichannel Sequencing Decision: SUGAR's two-year digital-only phase before entering offline retail was strategically deliberate. It allowed the brand to build a loyal digital customer base, prove demand, and generate data on which SKUs had strongest commercial traction before investing in offline inventory risk and retail margins. When SUGAR did expand offline, it did so with a product portfolio shaped by real purchase behaviour rather than manufacturer recommendations or retail buyer opinion. The counter-cyclical offline expansion during the pandemic — continuing to open stores while competitors contracted — reflects a conviction that offline share of colour cosmetics in India is structurally durable, and that periods of disruption offer distribution advantages to brands willing to hold the position.

Mid-Premium "Masstige" Positioning in a Polarised Category: The colour cosmetics category in India has historically been dominated at the mass end (Lakmé, Maybelline) and the premium end (MAC, international prestige). SUGAR's occupation of the mid-premium space — quality-forward, India-formulated, aspirationally branded, but accessible — reflects a strategic insight about the Indian beauty consumer's aspirational identity exceeding her current income level. The "affordable luxury" or masstige position is inherently vulnerable to compression from both ends (mass brands premiumising, and premiums discounting), and SUGAR's ability to sustain it will depend on continued product innovation and brand distinctiveness.

Founder Visibility as Brand Asset: Vineeta Singh's participation in Shark Tank India from Season 1 has created a dimension of brand equity that is difficult to quantify but impossible to replicate through advertising spend. The public identification of the brand with its founder's values, aesthetic sensibility, and entrepreneurial credibility has built trust — particularly in Tier 2 and Tier 3 markets where SUGAR's offline expansion is concentrating. This founder-brand fusion is a feature of brand architecture that strategic planners must consider as both an asset and a risk (founder reputation and brand reputation become structurally linked).

The Path to Profitability: SUGAR's FY24 financial results — 20% revenue growth combined with an 11.3% reduction in net losses — suggest a business that is beginning to optimise its cost structure as offline scale generates improved per-store economics. With advertising spend essentially flat between FY23 and FY24 (Rs 162.6 crore to Rs 161.6 crore) while revenue grew 20%, the marketing efficiency ratio is visibly improving. The IPO ambition makes the profitability trajectory strategically important: institutional investors will require demonstrated operating leverage before a public listing, and the FY24 trajectory is a meaningful first data point.

Discussion Questions

Consumer Intelligence and Competitive Advantage: SUGAR's founders derived their founding consumer insight from FAB BAG, a structurally different but adjacent business. How replicable is this "pre-launch research as prior business" model? Under what conditions can a brand entering a new category generate equivalent consumer intelligence without the benefit of an existing customer base? What are the risks of over-indexing on insights from a subscriber cohort when building a brand for a broader mass market?

Content vs. Performance Marketing Trade-off: SUGAR's conscious de-prioritisation of performance marketing in favour of brand content is strategically distinctive but difficult to evaluate in the short term. How should a D2C brand construct its marketing attribution framework to measure the long-term equity contribution of educational content against the short-cycle conversions driven by performance advertising? At what point in a brand's lifecycle does this trade-off change — and should SUGAR's approach evolve as it approaches IPO?

Omnichannel Sequencing and the D2C Paradox: SUGAR launched digitally but generates approximately 65% of revenues offline. This is not a failure of digital strategy but an accurate reading of India's market structure. What does this imply for other D2C beauty brands that are treating digital-first as digital-permanent? Design the decision criteria a D2C brand should use to determine when, and at what pace, to invest in offline expansion — and what signals from digital performance data would trigger that decision?

Masstige Positioning Sustainability: SUGAR occupies a mid-premium "masstige" price band — above mass-market domestic brands but below international prestige players. As L'Oréal and HUL aggressively premiumise their existing brands (as evidenced by HUL's Lakmé hybrid makeup-skincare line), and as new-age D2C brands like RENÉE and Nykaa's own label compress the competitive space, how durable is SUGAR's masstige position? What product, pricing, or brand architecture decisions could sustain competitive distinctiveness in an increasingly crowded mid-premium tier?

IPO Readiness and the Growth-Profitability Tension: SUGAR's stated IPO ambition is conditioned on achieving Rs 1,000 crore in revenue and demonstrated profitability. FY24 revenue of Rs 505 crore and a net loss of Rs 67.58 crore suggest both targets remain work-in-progress. Analyse the strategic choices available to SUGAR to accelerate the path to profitability without sacrificing the growth momentum that justifies its ~Rs 4,100 crore valuation. Which levers — pricing, advertising efficiency, portfolio rationalisation, geographic concentration — offer the highest return on strategic attention in the near term?

Comments