Lenskart's Omnichannel Retail Integration Model

- 3 hours ago

- 10 min read

Industry & Competitive Context

India's eyewear industry was valued at approximately USD 9.2 billion in FY25 and is projected to grow at a compound annual rate of roughly 13%, reaching about USD 17.2 billion by FY30, according to a RedSeer report cited in Lenskart's Draft Red Herring Prospectus (DRHP) filed with SEBI in July 2025. Within this market, prescription eyeglasses account for close to 73% of value, followed by sunglasses (about 22%) and contact lenses (about 5%). Critically, the industry remains predominantly unorganised: organised retailers held only about 24% of the market in FY25, a share the DRHP projects will rise to roughly 31% by FY30 as supply chains professionalise and omnichannel formats spread. Lenskart's own market-sizing methodology has been publicly contested. Titan Eye+ has stated its estimate of the addressable eyewear opportunity at closer to USD 3.4 billion, based on a narrower, organised-sector-only view, versus Lenskart's broader USD 9.2 billion estimate that includes unorganised sales and latent, uncorrected-vision demand (reported by TechStory, November 2025, and corroborated by Lenskart's own DRHP disclosures). This divergence is itself informative: it reflects two different theories of where growth will come from — deepening share within existing organised demand (Titan's frame) versus converting first-time, unaddressed vision-correction need (Lenskart's frame). On the competitive landscape, Lenskart's DRHP explicitly states that no listed company in India or globally shares its exact integrated business model. It names Titan Company Limited (through its Eyecare/Eye+ division) and regional chains such as Specsmakers and GKB Opticals as domestic competitors, and identifies EssilorLuxottica, Fielmann, JINS Holdings, and Warby Parker as global comparables (as reported by IndMoney's IPO coverage of the DRHP). Titan Eye+ reported domestic eyewear revenue of about ₹786 crore in FY25 from roughly 900 stores, compared with Lenskart's much larger revenue base and store network — though Titan operates at steadier double-digit margins under the Tata Group umbrella, drawing on decades of trusted brand equity (TechStory, November 2025). This sets up the industry's central strategic tension: Lenskart's scale-and-technology-led model versus legacy retailers' brand-trust-and-discipline model.

Brand Situation Prior to the Omnichannel Shift

Lenskart was founded in 2010 (with its corporate entity established in 2008) by Peyush Bansal, Amit Chaudhary, Sumeet Kapahi, and Neha Bansal, initially as an online-only direct-to-consumer eyewear retailer. According to company statements reported in The Economic Times and other business publications, Lenskart introduced a "home trial" service around 2011–2012, allowing customers to select frames online and receive multiple pairs at home to try before purchase — an attempt to solve the core barrier to buying prescription eyewear sight-unseen over the internet. Despite this innovation, purely digital distribution proved insufficient to scale eyewear, a category with an inherent need for fit, prescription accuracy, and tactile trial. According to an account in Outlook Business (2019), Lenskart began opening physical stores from around 2012 and scaled this offline push materially from 2015 onward — at which point the company had approximately 1.5 million customers. From 2015, Lenskart added an average of about 13 stores per month; by the time of that 2019 report, offline transactions already contributed roughly 75% of overall business, even though the company had built its identity as a digital-first brand. Company executives, in interviews with Outlook Business, stated that in-store conversion rates ran at approximately 30% compared with about 5% online, and that average in-store bill values ran roughly 1.8 times higher than online transactions — illustrating why a channel pivot became commercially necessary rather than optional. A separate Indian Retailer report describes an earlier phase of this expansion, in which Lenskart — then operating 70 stores across 29 cities through franchisees — announced plans to add 500 further outlets via the franchise route, split between exclusive stores and shop-in-shop formats. This reflects a deliberate, capital-light route to physical scale in the earlier years, before the company later shifted toward a larger mix of company-owned, company-operated (CoCo) stores as it matured.

Strategic Objective

Based on public statements by co-founders Peyush Bansal and Amit Chaudhary reported across The Economic Times, Business Standard, Mint, and The Ken, Lenskart's stated strategic intent was not to run two separate businesses (an e-commerce arm and a retail chain) but to build a single, technologically unified retail system in which inventory, customer data, and service could move seamlessly across digital and physical touchpoints. Chaudhary is reported by Outlook Business to have stated the company's ambition to achieve a significantly higher share of the Indian eyewear market than was achievable through an online-only model, explicitly noting that this could not be accomplished "only with an online presence." The objective, as documented across these sources, had three connected components: (i) use physical stores to solve the trust, trial, and prescription-accuracy problems that constrain online eyewear sales; (ii) use the online platform and app to extend reach, drive discovery, and gather data that improves store siting and merchandising; and (iii) back both channels with in-house manufacturing and a centralised supply chain to protect margins while keeping prices low enough to convert first-time, price-sensitive buyers away from unorganised local opticians.

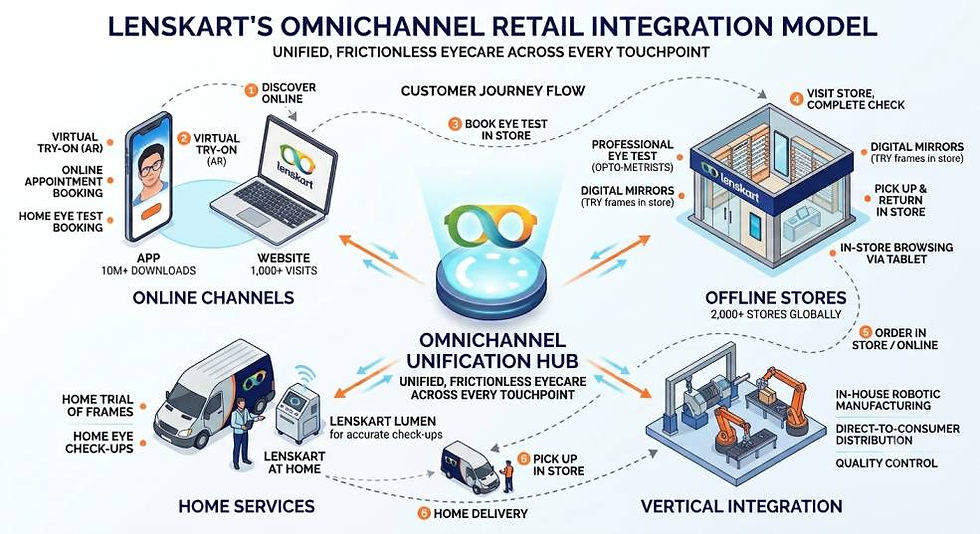

Omnichannel Architecture & Execution

Vertical integration as the operating backbone. Lenskart's DRHP and subsequent IPO-related disclosures describe centralised manufacturing facilities in Bhiwadi and Gurugram (India), Singapore, and the United Arab Emirates, supplemented by production through a joint venture in China. This backward integration into frame and lens manufacturing is positioned by the company as the mechanism that allows it to price aggressively across both channels without eroding margins.

Store network and format mix. As of March 31, 2025, Lenskart operated 2,723 stores globally — 2,067 in India and 656 overseas — of which, in India, 1,757 were company-owned and 310 were franchised, per the DRHP as cited in IPO analyses (Chittorgarh, Finology). By June 30, 2025, the network had grown to 2,806 stores globally (2,137 in India and 669 international), according to IndMoney's summary of updated DRHP disclosures. Historically, roughly 40% of the Indian store base operated on a franchise model, under which Lenskart supplied store design, inventory, technology systems, training, and marketing while franchise partners funded store setup — a structure the company has used particularly for expansion into Tier 2/3 cities (Outlook Business; Franchise India, as referenced in company statements).

Technology layer connecting the channels. The DRHP and subsequent reporting describe several proprietary technology capabilities: AI-enabled virtual try-on tools (with 3.86 crore/38.6 million virtual try-on sessions recorded in FY25, per DRHP-sourced figures cited by IndMoney and TechStory); computer-vision tools used for store layout optimisation; and geo-analytics used to guide new store site selection. The company's mobile applications had crossed 100 million cumulative downloads as of the DRHP filing period. According to TechStory's November 2025 coverage of DRHP disclosures, digital channels (including the app) contributed a significant share of overall sales, with virtual try-on cited by CEO Peyush Bansal as a meaningful driver of digital conversion.

Loyalty and repeat-engagement infrastructure. The Lenskart Gold loyalty programme had 71.2 lakh (7.12 million) members in India as of June 30, 2025, per DRHP disclosures reported by IndMoney. The DRHP also disclosed that new customers acquired in FY23 purchased eyeglasses at a higher average frequency over two years than the broader Indian market average, though the underlying comparison methodology was not detailed beyond what appears in the DRHP summary.

Eye-testing as a channel-agnostic service layer. Per DRHP figures cited by TechStory, the number of eye tests conducted by Lenskart rose from about 5 million in FY23 to about 13 million in FY25, with roughly 46% of FY25 tests being for first-time examinees — data the company has used publicly to argue that its store network is expanding the addressable market rather than merely capturing existing organised demand.

Brand portfolio segmentation. The DRHP describes a tiered brand architecture spanning value-oriented lines (such as Vincent Chase) to premium positioning (such as Owndays, the Japanese eyewear chain Lenskart owns and operates, and John Jacobs), allowing the same store and platform infrastructure to serve multiple price segments and customer profiles under one operating system.

Positioning & Consumer Insight

The consumer insight underlying Lenskart's model, as consistently described in Bansal's and Chaudhary's public statements, is that eyewear is a category where digital convenience and physical reassurance are complements, not substitutes. A customer might discover a frame and check pricing online, but still wants a professional eye test, a fit check, and same-day or next-day physical possession of a corrective product — needs a pure e-commerce model cannot satisfy at scale. Outlook Business quotes Chaudhary's description of the store experience as designed to let a customer "browse" a physical store the way they would browse online, without pushy sales interference, positioning the store as an extension of the digital interface rather than a distinct retail format.

A second, related insight — repeatedly surfaced in the DRHP's market-sizing argument and in Bansal's public comments (as reported by TechStory) — is that India's real constraint is not competition for existing organised demand but the sheer size of uncorrected vision need in the population. By emphasising eye-test volumes and the share of first-time test-takers, Lenskart has publicly framed its store network less as retail square footage competing for existing eyewear spend and more as a distribution mechanism for a public-health-adjacent, underpenetrated need — a framing that also shapes how it justifies its higher market-size estimate relative to Titan's.

Media & Channel Strategy

Public disclosures on paid media and demand-generation strategy are limited chiefly to what the DRHP states about planned use of IPO proceeds. Lenskart earmarked ₹320.06 crore of its ₹2,150 crore fresh issue specifically for "brand marketing and business promotion expenses to enhance brand awareness," against total FY25 marketing and promotion expenses of ₹448.41 crore, as disclosed in the DRHP and reported by IndMoney. Beyond this, no verified public information is available on specific advertising campaign creative, media mix allocation (television versus digital versus outdoor), influencer partnerships, or campaign-level performance metrics; company disclosures at the level available here are financial and operational rather than creative or media-planning in nature.

Business & Brand Outcomes

Lenskart's operating revenue rose from ₹5,427 crore in FY24 to ₹6,652 crore in FY25, an increase of approximately 22.6% year-on-year, per the DRHP as widely reported (PL India, Paytm Money, IndMoney). FY25 marked the company's first full-year net profit, at ₹297 crore, compared with a net loss of ₹10 crore in FY24. Gross margin stood at approximately 70% in FY25, and EBITDA margin at 14.6%, with Return on Capital Employed (ROCE) of 13.84%, according to DRHP figures cited by Paytm Money's IPO coverage. Net worth stood at ₹6,108.30 crore as of March 31, 2025, and total borrowings had been reduced from ₹917.21 crore (March 2023) to ₹345.94 crore (March 2025), later reported at ₹335.48 crore as of June 30, 2025. On store-level productivity, the DRHP disclosed that new stores achieved an average payback period of 10.29 months across metropolitan and Tier 1/2+ Indian cities as of March 31, 2025, and that Indian stores recorded average annual sales of ₹23,492.5 per square foot in FY25 — described in DRHP-based reporting (IndMoney) as the highest among organised eyewear rivals in India, though the specific comparison set was not itemised in the sources reviewed. Lenskart is documented, per RedSeer data cited in the DRHP, as India's largest seller of prescription eyeglasses by volume in FY25, with a stated market share of approximately 4–6% of India's overall prescription eyewear market and a store footprint reported to be roughly 2.5 times larger than the next-largest organised competitor. On the transaction that made these disclosures public: Lenskart filed its DRHP with SEBI on July 29, 2025, targeting a ₹2,150 crore fresh issue plus an offer for sale of 132.28 million shares by existing investors. The IPO opened for subscription on October 31, 2025, and closed on November 4, 2025, priced in a band of ₹382–402 per share; shares listed on the NSE and BSE on November 10, 2025. The total issue size was ₹7,278 crore, and post-issue market capitalisation was reported at approximately ₹69,726.83 crore (roughly USD 7.9–8 billion). Prior to listing, the company had raised over USD 1.08 billion across 19 funding rounds from investors including SoftBank, Temasek, TPG, Chiratae Ventures, Kedaara Capital, KKR, and ChrysCapital, according to DRHP-based reporting.

Strategic Implications

Lenskart's trajectory illustrates a pattern relevant to omnichannel strategy more broadly: a digital-native retailer's physical footprint is not necessarily a hedge against its online model but can be engineered as the primary conversion and trust-building mechanism for a category where trial, fit, and professional service matter as much as price or convenience. The documented shift from online-only to a franchise-led offline build-out, and later to a larger owned-store mix, shows a company sequencing its channel investment to match its balance-sheet maturity — starting capital-light through franchising, then shifting toward company-operated stores once IPO-stage capital became available for expansion, as reflected in the DRHP's stated use of proceeds. The public dispute with Titan Eye+ over total addressable market size is itself a strategically instructive data point: it shows how the same industry data can be interpreted through two different growth theses — organised-share capture versus category expansion — and how such framing choices can materially affect how investors value a pre-IPO or newly listed omnichannel retailer. Similarly, the disclosed store payback period (10.29 months) and per-square-foot productivity figures, taken together with the vertical integration into manufacturing, indicate a deliberate strategy of using owned production economics to fund an unusually dense and fast-payback retail expansion — a combination not typically available to retailers that do not control their own supply chain. Finally, Lenskart's own DRHP assertion that no listed peer replicates its exact combination of manufacturing, technology, and omnichannel retail is a claim investors and competitors alike will test over time, particularly as the organised share of India's eyewear market grows from roughly 24% toward the DRHP's projected 31% by FY30, and as legacy players such as Titan Eye+ and international entrants such as EssilorLuxottica compete for the same expanding, still largely unorganised demand pool.

Discussion Questions

Lenskart shifted from an online-only D2C model to a franchise-led, then increasingly company-owned, physical retail network. What criteria should a digital-native retailer use to decide the optimal sequencing between franchised and company-operated store formats as it scales?

Lenskart and Titan Eye+ have published materially different estimates of India's total addressable eyewear market (USD 9.2 billion versus USD 3.4 billion). What does this divergence reveal about the role of market-sizing assumptions in shaping IPO valuation narratives, and how should investors evaluate competing TAM claims from an issuer versus an independent competitor?

Lenskart discloses very high gross margins (~70%) driven by vertical integration into manufacturing, alongside comparatively thinner EBITDA margins (14.6%). What are the strategic trade-offs of owning manufacturing and inventory in a retail model versus relying on third-party supply, particularly with respect to capital intensity and operating leverage?

The DRHP frames Lenskart's rising eye-test volumes and high share of first-time test-takers as evidence of category expansion rather than pure market-share capture from competitors. How should this claim be evaluated strategically, and what kind of independent evidence would strengthen or weaken it?

Lenskart's franchise model provided store design, inventory, technology, and training to franchise partners, particularly in Tier 2/3 cities. What are the risks and benefits of using franchising as a scaling mechanism for a company whose core differentiation rests on integrated technology and centralised supply chain control?

Comments