Zepto’s Hyperlocal Fulfillment Strategy

- 2 hours ago

- 11 min read

Industry and Competitive Context

India's retail market, valued at approximately $1.1 trillion by TechCrunch-cited estimates, has long been fragmented across millions of small, family-owned kirana stores. The pandemic-era shift toward digital grocery ordering exposed a structural gap that traditional e-commerce platforms were poorly positioned to fill: consumers in dense urban India wanted not just convenience, but immediacy. This demand created the category now known as quick commerce, or q-commerce — the delivery of daily essentials within ten to thirty minutes of order placement.

The Indian quick commerce market grew from a GMV of approximately $500 million in FY 2021–22 to $3.34 billion in FY 2023–24, representing annual growth of approximately 73 percent, according to data compiled by India Briefing citing the Chryseum report. By 2024, quick commerce platforms had captured over two-thirds of all online grocery orders in India, according to RedSeer. The market is forecast to continue expanding at roughly 40 percent annually through 2030, with Morgan Stanley projecting the sector could reach $42 billion by that year.

The competitive structure that emerged by 2024 was essentially a three-player market: Blinkit (owned by Zomato, now rebranded Eternal), Swiggy Instamart, and Zepto. A November 2024 estimate from Motilal Oswal placed Blinkit at approximately 46 percent market share, Zepto at 29 percent, and Instamart at 24 percent. By September 2025, Bank of America research indicated Blinkit had crossed 50 percent, with Zepto and Instamart competing for the second position. The structural advantage Blinkit holds flows partly from its parent company's balance sheet and established consumer relationships through Zomato's food delivery platform. Zepto, by contrast, entered this race as an independent, venture-backed startup without an existing consumer app or logistics infrastructure to leverage.

Dark stores — compact, consumer-inaccessible micro-warehouses located within two to three kilometres of high-density residential clusters — had become the defining infrastructure of this category by 2023. According to HSBC Global Research cited by Business Standard, the total number of quick commerce dark stores across India grew from approximately 1,800 at the end of FY24 to over 4,000 by FY25, with projections of 5,500 by FY26. By the close of 2024, Blinkit had scaled to over 1,000 dark stores, Swiggy Instamart had 609 as of the September 2024 quarter, and Zepto had reportedly reached 700 to 750 dark stores as of November 2024.

Brand Situation Prior to Strategy Formation

Zepto was founded in July 2021 by Aadit Palicha and Kaivalya Vohra, then nineteen years old, after the founders paused their enrollment at Stanford University. The company originated as KiranaKart, a service that partnered with existing neighborhood kirana stores to facilitate delivery. That model did not gain sufficient traction, and in 2021 the company rebranded to Zepto and made a foundational strategic shift: rather than depending on third-party store inventory and fulfillment, it would build and operate its own network of dedicated dark stores.

The name Zepto was derived from the scientific prefix for a trillionth of a billionth — an unmistakable declaration of the company's core service promise. Zepto raised $60 million in October 2021 led by Nexus Venture Partners and Y Combinator, followed by $100 million in December 2021 and $200 million in May 2022. These rounds funded the initial dark store buildout across India's major metros. The company was accepted into Y Combinator's accelerator program while still developing the early platform.

At entry, Zepto faced two established competitors: Swiggy Instamart, which benefited from Swiggy's existing delivery workforce and brand recognition, and Blinkit (formerly Grofers), which had already pivoted to quick commerce and subsequently secured the powerful backing of Zomato. Zepto's strategic situation demanded that it establish meaningful differentiation through infrastructure density and operational precision, because in a category where the product is essentially time, the company that controls fulfillment end-to-end holds the most defensible position.

Strategic Objective

Zepto's stated and demonstrable strategic objective was to build a vertically integrated hyperlocal fulfillment system capable of consistently delivering orders within ten minutes, and to achieve this at a scale and density that would generate sustainable unit economics in mature markets before expanding to new geographies. This was not merely a logistics ambition. It was a market-making bet: that by reliably delivering in ten minutes or fewer, Zepto could re-condition urban Indian consumers away from kirana stores and traditional e-commerce alike, establishing a new behavioral norm from which it would be the primary beneficiary.

This objective had a financial corollary. Co-founder Aadit Palicha publicly indicated that Zepto had reported a 44 percent year-on-year improvement in EBITDA percentage in calendar year 2023, and expressed confidence that the company would turn EBITDA positive in 2024 — approximately within 36 months of launch, per analysis by JM Financial. The pursuit of profitability at the dark store level was not incidental; it was the mechanism by which Zepto intended to demonstrate that speed and unit economics were compatible, a proposition the broader investor community remained skeptical about during the funding contraction period of 2022.

Campaign Architecture and Execution: The Hyperlocal Fulfillment System

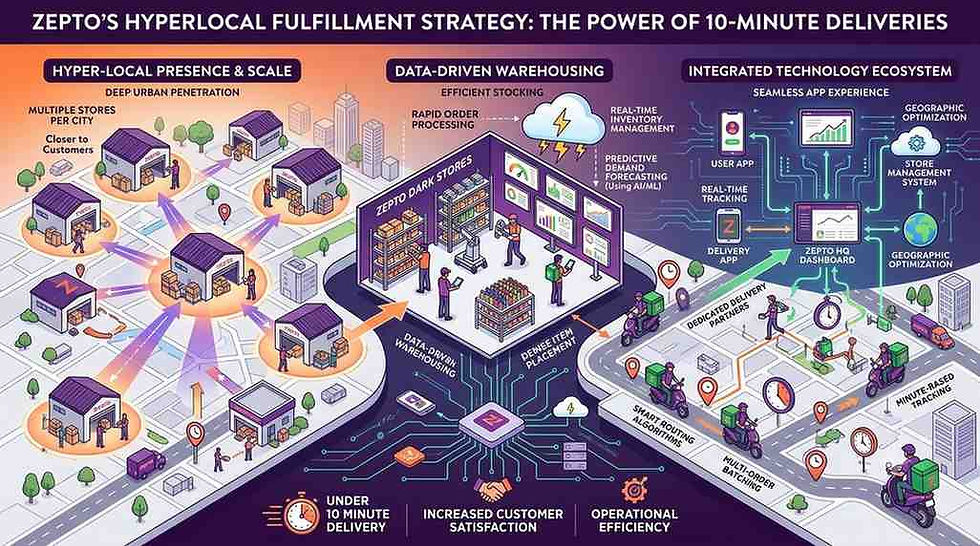

Zepto's hyperlocal fulfillment strategy was built around three interlocking operational pillars: physical infrastructure density, internal supply chain verticalization, and technology-driven coordination.

On infrastructure, Zepto made the deliberate choice to own and operate its dark stores rather than rely on third-party warehouse partners. Each dark store occupies between 2,000 and 4,400 square feet, is closed to consumers, and is positioned within two to three kilometres of a target customer cluster, as documented by multiple operational analyses of the platform's structure. By the first quarter of 2024, Zepto had operationalized over 300 dark stores across major Indian cities, according to reporting by 42signals. By November 2024, that number had reportedly reached 700 to 750 stores. As of the October 2025 TechCrunch report following Zepto's latest funding round, the company had over 1,000 dark stores in operation across major cities, with plans to add hundreds more over the subsequent twelve months.

The stores themselves were optimized not for storage breadth but for picking speed. Zepto maintained a curated catalog of approximately 2,500 to 3,000 SKUs per dark store, stocking only high-velocity, high-frequency items rather than attempting the comprehensive assortment of a traditional supermarket. The store layout placed high-demand products — staples, dairy, snacks, personal care — closest to packing zones to minimize picker movement per order. Co-founder Aadit Palicha stated publicly that within 76 seconds of an order being placed, the order is packed and made ready for pickup. This operational standard was reinforced through store layout design, SKU placement decisions, and picker training protocols.

On supply chain verticalization, Zepto maintained full control of its last-mile delivery fleet rather than routing orders through third-party logistics providers. Delivery partners were stationed at dark stores and were assigned orders before picking was even completed, ensuring that the handoff between fulfillment and dispatch was nearly instantaneous. As of its June 2024 funding round, Zepto disclosed that it worked with more than 50,000 delivery partners and was adding more than 5,000 new delivery partners each month.

In 2024, Zepto also registered "Zepto Marketplace Private Limited" in October 2024 to transition elements of its model to a franchise structure, allowing third-party operators to manage day-to-day store operations under Zepto's standard operating procedures and technology stack. This hybrid ownership approach was designed to accelerate geographic expansion while managing the capital intensity of direct store ownership.

On category expansion, Zepto launched Zepto Cafe in April 2022 as a cloud kitchen initiative operating within existing dark stores, offering hot beverages and ready-to-eat food. By 2025, the company reported a Zepto Cafe annualized run rate exceeding $110 million, though it had temporarily paused the service in 44 cities due to staffing challenges before resuming. Zepto also launched Zepto Bloom in February 2023, a platform enabling farmers to manage food production and distribute produce from villages to cities, creating a backward integration component to its supply chain.

Positioning and Consumer Insight

Zepto's foundational consumer insight was that Indian urban consumers — particularly millennials and young professionals in metro cities — did not merely prefer fast delivery as an incremental improvement over existing options. For a specific set of high-frequency, low-ticket purchase occasions, speed was the entire value proposition. The use case was not the planned weekly grocery run; it was the missing ingredient needed immediately for cooking, the household staple discovered to be out of stock, the late-night craving. In these moments, waiting two hours was functionally equivalent to not having the product at all.

This insight drove Zepto to position itself not as an online grocery store competing on assortment or price, but as infrastructure — a utility as immediate and reliable as running water. The ten-minute promise became the brand's entire positioning architecture. The company name itself encoded this positioning: zero latency was the aspiration, and every operational decision was oriented toward that benchmark.

On marketing execution, Zepto pursued a dual strategy of performance marketing for acquisition — app-install campaigns and first-order discount promotions targeting urban millennials — combined with brand-building investments as the category matured. In 2024 and 2025, the company expanded into brand sponsorships, including an IPL sponsorship and celebrity brand ambassador campaigns, reflecting a deliberate shift from pure performance marketing toward building top-of-mind awareness. This shift was strategically significant: in a category where Blinkit benefits from Zomato's existing brand equity, Zepto needed to build standalone recognition. In February 2024, Zepto launched a paid membership program. By April 2024, the membership program had exceeded four million subscribers, according to Wikipedia's documented timeline citing public sources.

Media and Channel Strategy

No verified public information is available on Zepto's specific media planning budget allocation, media mix weightings, or the precise breakdown of marketing expenditure by channel. What is publicly documented is the following: Zepto concentrated its consumer acquisition through its own app as the primary interface, reflecting the broader category pattern in which app downloads served as the main proxy for consumer reach. Zepto led the competitive set on this metric, with nearly 11 million downloads across Google Play and the Apple App Store at the time of India Briefing's documented analysis. Swiggy's app, which bundled both Instamart and food delivery, had approximately 9.8 million downloads, while Blinkit had roughly 6.6 million.

Zepto also built Zepto Atom, launched in early 2024, as a proprietary analytics platform providing FMCG brand partners with real-time data on product performance and consumer behavior. This platform represented a meaningful B2B revenue stream — brands paying for visibility and data access on the Zepto network — while simultaneously reinforcing Zepto's positioning as a technology-first platform rather than a conventional grocery retailer.

Business and Brand Outcomes

The financial trajectory documented through public sources reflects a company that achieved extraordinary revenue growth while continuing to operate at a loss, a pattern consistent with the infrastructure-heavy, market-share-first approach that has characterized Indian q-commerce.

Zepto's revenue grew 149 percent to approximately Rs 11,100 crore in FY25 from Rs 4,454 crore in FY24, according to Inc42's reporting on the October 2025 funding round announcement. At the same time, the company's losses reportedly widened to approximately Rs 3,367 crore in FY25 from Rs 1,215 crore in FY24, as reported by CNBC. Achieving profitability at a company level remains an outstanding challenge.

At the unit level, however, the picture was more encouraging. Zepto disclosed in June 2024, at the time of its Series F round, that approximately 75 percent of its dark stores were EBITDA positive as of May 2024. The company also disclosed that the time required for a dark store to achieve profitability had improved dramatically — a store that previously took 23 months to turn EBITDA positive was reaching that milestone in approximately six months. This improvement in store-level maturation curves was presented by the company as evidence of improving operational leverage as the network scaled.

The company's valuation trajectory confirmed sustained investor confidence. From a $900 million valuation in December 2022, Zepto reached $1.4 billion unicorn status in May 2023, $3.6 billion in June 2024, $5 billion in August 2024, and $7 billion in October 2025 when it raised $450 million in a round led by CalPERS, the California Public Employees' Retirement System. Total capital raised exceeded $2.3 billion across multiple rounds, with over $1 billion raised in 2024 alone. Following co-founder Aadit Palicha's public statement at the time of the October 2025 round, the company held approximately $900 million in net cash on its balance sheet. By December 2025, Zepto had confidentially filed for an IPO targeting $1.22 billion in fresh capital, according to CNBC.

Strategic Implications

Zepto's hyperlocal fulfillment strategy carries several implications that are analytically significant beyond the company's specific case.

The first is the identification of speed as a category-defining rather than merely differentiating attribute. In most retail contexts, speed of delivery is one variable among several, including price, selection, and quality. Zepto's operational thesis was that within a specific band of urban consumer occasions, speed was the only variable that mattered. This allowed the company to make radical trade-offs that would be counterproductive in conventional retail — sacrificing assortment breadth for picking speed, sacrificing geographic reach for network density, sacrificing short-term profitability for the infrastructure density required to make the service promise credible.

The second implication concerns the relationship between infrastructure density and competitive moat. Zepto's architecture is defensible not because it is technologically proprietary in a narrow sense, but because it requires enormous capital investment to replicate at the density necessary to be operationally viable. A competitor entering a city must reach a critical threshold of dark store density before the network generates reliable delivery times — below that threshold, the service promise cannot be maintained, and the consumer proposition collapses. This creates a winner-takes-most dynamic within defined geographies, where the first mover to achieve density holds a structural advantage that later entrants face significant capital barriers to overcome.

The third implication concerns the challenge of expanding this model beyond metros. Redseer's documented analysis found that orders per day per dark store dropped sharply below 1,000 beyond the top ten to fifteen Indian cities, and below 700 in the next twenty. The analysis further noted that breakeven throughput in smaller cities was 1.5 to 2 times higher than in metros, due to lower average order values and wider required delivery radii. This means the unit economics that underpin Zepto's metro profitability do not translate automatically to smaller geographies — a significant constraint on the company's addressable market as competition intensifies and all three major players seek growth beyond saturated metros.

The fourth implication relates to the sustainability of losses at scale. Blinkit CEO Albinder Dhindsa's public comments to Bloomberg, reported by CNBC, that the industry had relied on "relentless fundraising" to cover steep losses and would face limits on how long that could continue, point to a structural question that Zepto must answer as it approaches a public markets event: whether its revenue growth trajectory can converge with unit economics improvement fast enough to satisfy public market investors who apply materially different profitability expectations than private market backers.

Finally, Zepto's franchise model transition, initiated through the registration of Zepto Marketplace Private Limited in October 2024, signals a recognition that the fully vertically integrated model carries capital intensity constraints as a standalone company. Franchise operators absorbing infrastructure and staffing costs while operating under Zepto's brand, technology, and SOPs represents a hybrid that could accelerate store network expansion without equivalent balance sheet impact — though it introduces quality and SLA consistency risks that company-owned stores do not carry in the same way.

MBA Discussion Questions

Zepto made a foundational choice to own and operate its dark stores rather than partner with third-party warehouse operators, at the cost of significantly higher capital intensity. Under what market conditions does vertical integration in fulfillment infrastructure create durable competitive advantage, and when does it become a liability rather than an asset?

The quick commerce category in India has consolidated into a structure where the leader, Blinkit, benefits from the brand equity and consumer relationships of its parent company, Eternal (formerly Zomato). How should a standalone, venture-backed competitor like Zepto think about brand-building investment at different stages of category maturity, and what metrics would you use to evaluate whether the IPL sponsorship and ambassador campaigns represent an appropriate capital allocation?

Zepto's store-level maturation curve improved from 23 months to reach EBITDA positivity down to approximately 6 months by mid-2024. What operational and demand-side factors most plausibly explain this improvement, and what risks could reverse it as Zepto expands into smaller cities with structurally different economics?

Redseer's research indicates that non-metro cities contribute just over 20 percent of quick commerce GMV despite platforms operating in 100-plus cities. Given the breakeven economics documented for smaller geographies, what strategic criteria should Zepto use to decide which non-metro markets to enter, and in what sequence?

Zepto confidentially filed for an IPO in December 2025 despite widening net losses in FY25. How should the company's management frame the growth-versus-profitability tension for public market investors, and what evidence from the dark store maturation data and market share trajectory would constitute the most credible case for long-term value creation?

Comments