Justdial's Local Search Monetization Model

- 1 day ago

- 10 min read

Industry & Competitive Context

India's local search and business-discovery market emerged from the convergence of rapid urbanization, a deeply fragmented small and medium enterprise (SME) ecosystem, and the country's accelerating transition from print directories to digital platforms. In the mid-1990s, when Justdial was founded, businesses lacked a scalable, cost-effective channel to reach geographically proximate consumers. Yellow-page directories were the dominant discovery mechanism, but they were expensive to print, costly to update, and impossible to search in real time. The structural gap between the supply of local services and the discoverability of those services created the conditions for a new intermediary. As internet penetration expanded — and, crucially, as mobile internet became widely accessible — two distinct threats reshaped the competitive landscape that Justdial had built. First, global general-purpose search engines, particularly Google, moved aggressively into local search with products such as Google Search and Google Maps, offering free, algorithmically powered business listings through "Google My Business." Second, a set of well-funded vertical-specific platforms — Zomato for food, Practo for healthcare, Urban Company for home services, BookMyShow for ticketing — began winning high-intent, high-frequency consumer categories that had previously belonged to horizontal local search engines. This dual pincer — a well-resourced horizontal competitor on one side and nimble vertical specialists on the other — defines the structural challenge that has faced Justdial for much of the past decade. The company has had to simultaneously defend its network-effect advantages (the breadth of its listings database and brand recall) while finding ways to deliver monetizable value that free alternatives do not provide.

Brand Situation Prior to Strategic Evolution

Justdial was incorporated in 1996 by V. S. S. Mani and was originally built around a telephone-based directory model, using the easily memorable pan-India number 8888888888. The official website, justdial.com, launched in 2007, and the company subsequently expanded to mobile apps on Android and iOS. It listed on both the BSE (scrip code 535648) and NSE (ticker: JUSTDIAL) in 2013, becoming one of India's first consumer internet companies to go public. At its IPO, the offering was priced at ₹530 per share; by August 2014 the stock had reached ₹1,894.7 before declining to the triple digits in 2015, reflecting both early investor enthusiasm and the structural risks inherent in the business model. Through its growth years, Justdial invested heavily in building a field-sales force. According to publicly disclosed company information, it operated with more than 9,000 employees during the pre-pandemic period, including dedicated telesales personnel, field marketing staff, and direct sales representatives ("Justdial Ambassadors") who approached SMEs across 250-plus cities covering more than 11,000 pin codes. This ground-level salesforce was the primary mechanism for converting free listings into paid subscriptions — a fundamentally people-intensive, rather than technology-driven, growth engine. The company also attempted to expand its revenue model beyond listing fees. It launched "Search Plus," an online marketplace and meta-search engine with transaction capabilities, and "JD Omni," a business-management tool for SMEs that included inventory management, billing, and website creation. Neither product achieved material scale, as publicly acknowledged through management commentary and credible news reporting. This reinforced the company's dependence on its core paid-listing revenue stream at a time when competitive intensity was escalating.

Key Pre-Transition Metric: As of 2020, Justdial reported approximately 29.4 million total listings and 536,236 active paid campaigns, with approximately 10,984 employees. Revenue for FY2020 stood at ₹1,092.81 crore, representing the pre-pandemic high-water mark. (Source: Wikipedia / Justdial public filings)

Strategic Objective

Justdial's core strategic objective, consistently stated across its public communications, is to build a scalable, recurring-revenue monetization model centered on converting free business listings into paid subscriber relationships. This objective operates across two axes. On the demand side, the goal is to grow quarterly unique visitors sufficiently to demonstrate reach and influence to paying advertisers. On the supply side, the goal is to increase the number of active paid campaigns and the average revenue realization per campaign. Following the July 2021 acquisition of a 66.95% stake by Reliance Retail Ventures Limited for ₹34.97 billion — one of the most significant structural events in the company's history — the strategic objective broadened to include integration with Reliance's commerce infrastructure. The deal terms, as publicly documented, included an agreement for Justdial to provide Reliance access to its merchant database. V. S. S. Mani was retained as Managing Director and CEO. Reliance's stated rationale included gaining exposure to Justdial's established SME salesforce relationships and its B2B portal JD Mart, which connects manufacturers, distributors, and wholesalers. The post-acquisition phase reflects a dual objective: financial recovery from pandemic-era contraction, and a longer-term transition from a pure listing-fee model toward a more diversified monetization architecture that includes lead generation, transactional revenue, and generative AI-enhanced search.

Monetization Architecture & Execution

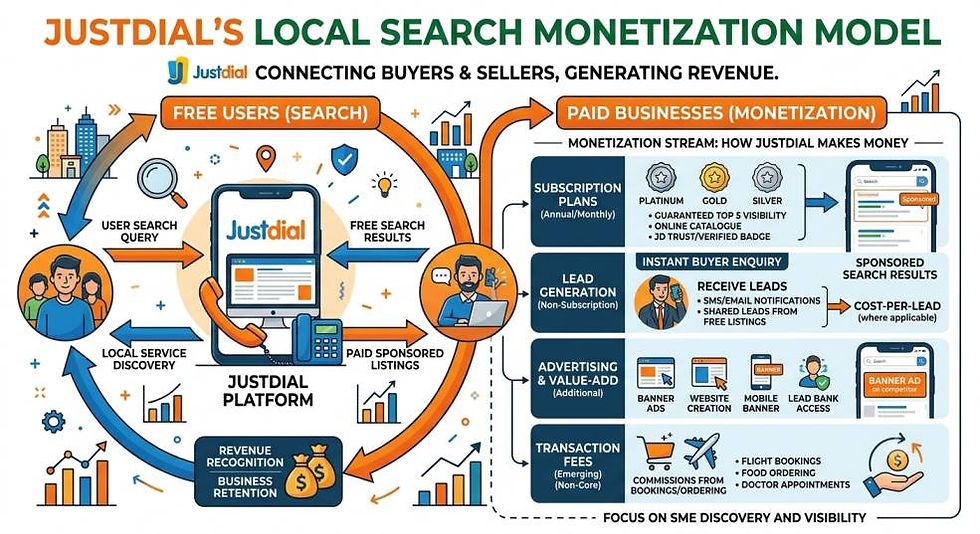

Justdial's revenue model is not built around discrete marketing campaigns in the conventional sense. Instead, it operates as a persistent, platform-level monetization architecture with three documented revenue streams.

Paid Listings and Premium Visibility

The primary revenue mechanism is subscription-based premium listing. Businesses in Justdial's database are listed free of charge by default. Paid subscribers receive enhanced visibility in search results — a higher ranking position, richer media (images, descriptions), and badges — relative to unpaid listings. This is structurally equivalent to a sponsored-search model, but implemented as a time-bound subscription rather than an auction-based cost-per-click system. The SME pays a fixed annual or quarterly fee for a defined tier of visibility, making revenue predictable for Justdial but decoupled from actual lead volumes delivered.

Cost-Per-Lead (CPL) Packages

For service-intensive categories — including pest control, interior decoration, packers and movers, laptop repairs, and RTO services — Justdial operates a lead-distribution model. Service providers purchase lead packages, and incoming consumer queries in those categories are distributed among a set of competing providers (typically four to seven businesses per query). This model monetizes consumer intent more directly and aligns Justdial's revenue more closely with the value delivered to the SME.

Advertising and Display

Justdial also sells display advertising on its platforms to businesses seeking broader brand exposure. This is a secondary revenue stream relative to paid listings but forms part of the overall advertiser value proposition. Execution of the merchant acquisition strategy relies heavily on a direct salesforce. Publicly disclosed company information confirms the importance of field teams ("feet-on-street") in onboarding SMEs, supplemented by a telesales function that pre-qualifies leads and schedules in-person meetings. In more recent filings and management commentary, Justdial has disclosed the addition of self-sign-up digital channels, which are intended to reduce friction for smaller or digitally native SMEs who may not want to engage a sales representative. On the consumer side, Justdial has maintained an omnichannel presence spanning the 8888888888 voice service, the website, and mobile apps. According to verified company data, over 86% of traffic originates from mobile platforms as of FY25, underscoring the strategic priority of the mobile-first experience.

Positioning & Consumer Insight

Justdial's positioning is built on three pillars: comprehensiveness, trust, and proximity. The platform's value proposition to consumers rests on the assertion that it provides the broadest, most verified database of local businesses in India. Justdial's official company overview describes its mission as providing "fast, free, reliable, and comprehensive information to our users and enable discovery and transactions for all products and services." The consumer insight underlying Justdial's model is straightforward: Indian consumers, particularly in non-metro markets, face severe information asymmetry when searching for local services. A consumer in a tier-2 city looking for a reliable electrician, a caterer, or a diagnostic lab has few reliable channels to evaluate options. Justdial's platform — combining verified contact information, user ratings, and proximity filters — reduces search friction in a way that was not possible through print directories or word-of-mouth alone. For merchants, the insight is symmetrical: local SMEs have limited digital marketing budgets, limited technical capacity to build their own online presence, and a high dependency on walk-in and word-of-mouth traffic. Justdial offers a managed, low-cost digital storefront with guaranteed consumer reach — addressing the digitization barrier directly. Justdial's official overview also highlights that it provides GST input credit and KYC capabilities to SME clients through its platform, adding compliance utility to its value proposition. The strategic tension in Justdial's positioning is that its primary competitor for consumer mindshare — Google — offers business listings free of charge, creating a credible free substitute for the consumer-side of Justdial's platform. Analyst commentary (as cited in public financial analysis) has consistently flagged Justdial's dependence on Google Search for driving traffic to its own platform as a structural vulnerability, representing a situation where the company is partially dependent on its primary competitor for distribution.

Media & Channel Strategy

Justdial has historically used a mix of traditional and digital media for brand building. Publicly available information confirms the use of television, print, and radio advertising, alongside digital channels. The company's branded voice number — 8888888888 — functioned as a marketing asset in itself, enabling high recall and direct response at minimal marginal cost per impression. For merchant acquisition, the primary channel is the direct salesforce, operating across more than 250 cities. The tiered salesforce structure — comprising telesales, field marketing staff, and Justdial Ambassadors — reflects a channel strategy calibrated to the heterogeneity of the SME market, where digital self-service penetration remains uneven. In recent years, the introduction of self-sign-up digital onboarding has been publicly noted as a strategic priority, representing a shift toward a lower-cost, scalable merchant acquisition channel.

Business & Brand Outcomes

Justdial's financial trajectory provides the most reliable basis for evaluating its monetization model's performance. The following figures are drawn from publicly disclosed financial results and credible financial reporting: Revenue declined from approximately ₹1,092 crore in FY2020 to ₹675 crore in FY2021 — a contraction of roughly 38% — primarily attributed to the pandemic's impact on SME advertising budgets. Recovery began in FY2022 (₹647 crore), accelerated in FY2023 (₹845 crore, approximately 30.6% year-on-year growth), continued in FY2024 (₹1,043 crore), and reached ₹1,141.9 crore in FY2025 — a 9.5% increase over FY2024. Net profit for FY2025 reached ₹584.2 crore, representing a 61% year-on-year increase.

Selected Verified Operating Metrics (FY2025):

— Quarterly Unique Visitors: 191.3 million (Q4 FY25), described as the highest reported quarterly figure in the company's history at that point, representing 11.8% year-on-year growth.

— Total Business Listings: 48.8 million as of March 2025 (vs. approximately 29.4 million in 2020).

— Q4 FY25 Revenue: ₹289.2 crore (+7% year-on-year).

— Q4 FY25 Net Profit: ₹157.6 crore (+36.3% year-on-year).

— EBITDA Margin (Q4 FY25): 29.8%.

On paid campaign metrics, public investor reporting notes that paid campaigns crossed 538,220 in Q4 FY2023, with an average realization of approximately ₹4,320 per campaign per quarter. Company management has publicly indicated that per-campaign pricing remains below pre-pandemic levels, framing current realization as having meaningful upside. In Q1 FY2024, the paid subscriber base publicly exceeded 5 lakh (500,000) accounts, a milestone cited by the company. An important caveat in interpreting Justdial's profitability: credible financial analysis has noted that a significant portion of Justdial's reported Profit Before Tax (PBT) comes from treasury income — earnings on the company's substantial cash reserves — rather than purely from operating revenue. This makes the bottom-line figures sensitive to interest rate cycles independent of the core advertising business's performance. On the listings database side, the growth from approximately 29.4 million listings in 2020 to 48.8 million in March 2025 (approximately 66% expansion in five years) reflects the platform's continued expansion of its supply base, though the proportion that are actively paid subscriptions versus free listings is not publicly disclosed in granular detail.

Strategic Implications

The Freemium Paradox in Local Search. Justdial's model depends on maintaining sufficient consumer traffic to justify SME subscription fees, while simultaneously competing with Google, which provides free business listings that reduce the perceived gap between Justdial's paid offering and a zero-cost alternative. The platform must continuously demonstrate that its paid listings deliver measurably better outcomes for advertisers than free Google My Business profiles — a proposition that is harder to defend for large, digitally sophisticated businesses than for smaller, less visible SMEs. This suggests a natural segmentation logic: Justdial's sustainable monetizable segment is concentrated among SMEs that lack the digital capability to optimize their own Google presence, which is itself a market segment subject to erosion as digital literacy improves.

Structural Fragility of SME-Dependent Revenue. The pandemic period demonstrated that when the core advertiser constituency faces existential financial pressure, subscription-based listing revenue can contract sharply — revenues fell nearly 38% between FY2020 and FY2021 — even when the consumer side of the platform continues to function. This procyclicality is an inherent feature of an SME-focused advertising model. Diversification toward transaction-based revenue (where Justdial earns a percentage of a completed service transaction rather than a fixed listing fee) would reduce this volatility, but no verified public information is available on the scale of Justdial's transactional revenue as of this writing.

The Reliance Leverage Question. The 2021 acquisition by Reliance Retail introduces a strategic option that was not previously available: the potential integration of Justdial's SME merchant database with Reliance's retail, payments, and logistics ecosystem. Management has publicly referenced this as a growth lever. However, the specific terms and current operational status of this integration have not been independently verified in public filings as of this writing, making it a strategic optionality rather than a documented outcome.

Vertical Disaggregation as a Persistent Threat. The entry of category-specific platforms — Zomato for dining, Practo for healthcare, Urban Company for home services — illustrates the canonical threat to horizontal aggregators: vertical specialists can offer deeper utility (reviews, booking, payment, service guarantees) within a single category, winning high-intent, high-frequency consumer behavior. Justdial's response — expanding into JD Mart (B2B), JD Pay (payments), and generative AI-enhanced search — reflects an attempt to deepen platform utility, though the publicly disclosed financial contribution of these extensions to total revenue remains limited relative to the core listings business.

AI as a Monetization Multiplier. Justdial has publicly disclosed the integration of Generative AI into its platform to improve query understanding, automate listing content enrichment, and enable conversational commerce. This represents a structurally important investment: if AI can improve search relevance and lead quality for paid subscribers, it strengthens the value proposition for SME advertisers without requiring proportional increases in the salesforce. Management commentary at the FY25 results announcement cited AI as a foundational element of the company's forward strategy — though, consistent with the guidelines of this case study, specific AI-driven revenue attribution is not yet verifiable from public sources.

MBA Discussion Questions

Two-Sided Marketplace Design: Justdial's model requires simultaneous growth on both the consumer (user) side and the merchant (advertiser) side. How should Justdial prioritize investment between these two sides in a resource-constrained environment, and what metrics would you use to diagnose which side of the marketplace is the binding constraint on growth?

Competitive Response to Google: Google My Business offers free local listings with high search visibility. Given that free vertical competitors can erode the supply side of Justdial's marketplace, what sustainable competitive advantages — if any — does Justdial possess that Google cannot easily replicate? Under what conditions does Justdial's paid-listing model remain defensible?

Revenue Model Transition: Justdial has historically earned fixed subscription fees rather than variable, transaction-linked revenue. Evaluate the trade-offs between subscription-based and transaction-based monetization for a local search platform serving India's SME segment. What conditions would make a transition to CPL or revenue-share models strategically preferable?

The Reliance Acquisition: Reliance Retail acquired a 66.95% stake in Justdial in 2021, granting it access to Justdial's merchant database. From a strategic marketing perspective, what are the potential synergies, and what are the risks that Justdial's independence — as a neutral local search platform — may be compromised in the eyes of its SME advertiser base?

Geographic Expansion vs. Depth: Historical financial analysis indicates that at Justdial's peak margins, more than 90% of revenue came from the top 11 cities. Subsequent expansion into tier-2 and tier-3 cities required lower pricing and yielded lower margins. How should Justdial recalibrate its geographic and pricing strategy in light of this evidence, and what product changes — if any — would make tier-2/3 markets more sustainably monetizable?

Comments