Licious’ Premium Fresh Food Business Model

- 2 hours ago

- 10 min read

Industry & Competitive Context

India's fresh meat and seafood market is simultaneously one of the country's largest food categories by consumption volume and one of its most structurally disorganised. Analysts at Bernstein estimate the total market opportunity at approximately $40 billion, yet for most of its history, this category has been served almost entirely through unregulated wet markets, roadside butchers, and informal distribution chains with no standardised quality controls, no cold-chain infrastructure, and no consistent hygiene benchmarks. With over 73 percent of India's population consuming meat, according to publicly reported figures, the market's scale was never in question. The central problem was structural trustlessness — consumers had no reliable mechanism to verify freshness, hygiene, or sourcing integrity.

Against this backdrop, a new wave of technology-first, direct-to-consumer startups emerged in the mid-2010s with a thesis that premium, trust-backed meat delivery could be a scalable consumer business. Competitors including FreshToHome, Zappfresh, and TenderCuts addressed overlapping consumer pain points. However, indirect competitive pressure has since expanded significantly. Quick commerce platforms, particularly Zepto, entered the branded meat space in 2023 with a proprietary brand called Relish. Swiggy and BigBasket have also served as distribution channels for fresh meat, though not always with the same quality positioning. The competitive dynamics of this category, therefore, are shaped not only by branded D2C challengers but by platform ecosystems that combine distribution speed with low barrier-to-entry for private labels.

In terms of funding leadership, Licious has maintained a significant advantage. It has raised approximately $490 million across twelve funding rounds, making it the highest-funded company in the branded fresh meat segment in India by a substantial margin. Its nearest funded competitor, FreshToHome, raised a cumulative $286 million as of 2023, including a $104 million round led by Amazon Sambhav Venture Fund. The capital gap between Licious and its peers has enabled deeper cold-chain infrastructure investment, broader geographic expansion, and a more intensive brand-building programme than any rival has been able to sustain at scale.

Brand Situation Prior to Strategic Pivot

Licious was founded in October 2015 by Abhay Hanjura and Vivek Gupta in Bengaluru, starting from a 3,000 square-foot processing facility with approximately 100 daily orders. Hanjura, an alumnus of BITS Pilani, brought product development and supply chain engineering expertise. Gupta, an alumnus of IIM Calcutta with prior experience at McKinsey and Rocket Internet, contributed business strategy and operational scaling capability. Their founding insight, publicly documented, was that two educated, urban consumers with purchasing power could not reliably access high-quality fresh meat in a major Indian metropolitan city — a problem that, if present at that income level, was structurally endemic across the market.

The company's early years were characterised by hyper-local supply chain construction rather than demand-side marketing. Licious built FSSAI-certified processing facilities, established direct sourcing relationships with farms and fisheries, and invested in refrigerated cold-chain logistics before attempting to scale demand. This sequencing — infrastructure first, brand later — was deliberate and consequential. It meant that Licious entered the consumer market with an operational proof point that competitors attempting to aggregate and rebrand third-party supply chains could not replicate quickly.

By the time of its Series F round in July 2021, led by Temasek and Multiples Alternate Asset Management, Licious reported year-on-year business growth of over 500 percent, attributable in part to the surge in online food consumption during the COVID-19 pandemic. The company disclosed that it had delivered to more than two million unique customers by October 2021. That same month, it raised $52 million in what was categorised as a Series G round, led by IIFL Asset Management's late-stage technology fund, achieving a valuation exceeding $1 billion and becoming India's first D2C unicorn in the fresh meat and seafood segment, as well as the twenty-ninth unicorn to emerge in India in 2021.

A subsequent $150 million fundraise in March 2022, led by Amansa Capital, Kotak PE, and Axis Growth Avenues, brought the all-time capital raise to approximately $488 million. Among the participants in that round were prominent investor-entrepreneurs including Nithin Kamath and Nikhil Kamath of Zerodha, as well as Aman Gupta of BoAt — a signal of its standing among India's new-generation business community.

Strategic Objective

Licious' stated strategic intent, documented across investor communications and press statements, has evolved across two distinct phases. In the first phase, spanning 2015 to 2022, the objective was category creation: establishing the existence and viability of a premium, trust-backed, D2C meat and seafood market in India. The company invested in brand communication that centred on hygiene, freshness guarantees, traceability, and the elimination of middlemen — not in competitive conquest but in consumer education.

In its second phase, which became more pronounced through FY23 and FY24, the strategic objective shifted to profitability through channel focus and omnichannel distribution. In a statement released alongside FY24 financial results, co-founders Hanjura and Gupta explicitly stated: "We are now focused on building a full-stack distribution operation through an omnichannel strategy. Last year has been a transition, with short-term impacts from strategic adjustments. However, we expect to see the positive results of these choices by the end of FY25." This communicates a deliberate trade of short-term revenue scale for structural unit economics improvement, a strategic choice with direct implications for IPO readiness.

The company has also publicly stated its ambition to expand its household reach from four million to thirty million, and its IPO intent within a twenty-four-month window from mid-2024, targeting a valuation in excess of $2 billion at listing.

Business Model Architecture & Execution

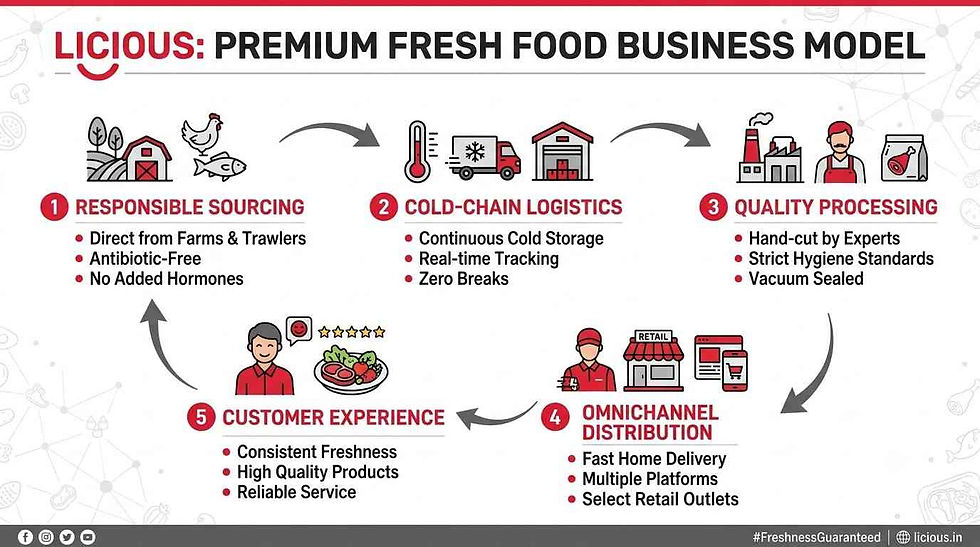

The defining strategic feature of Licious is full vertical integration across the fresh protein value chain. Unlike aggregator platforms that list and fulfil third-party inventory, Licious owns or directly controls procurement, processing, quality assurance, packaging, and last-mile delivery. This architecture is the basis of its premium positioning. In a category where the fundamental consumer barrier is trust, vertical integration functions not merely as an operational preference but as the primary brand communication mechanism.

Sourcing is conducted through long-term contracts with farms and fisheries, a practice the company confirmed it has deepened in the two years preceding its anticipated IPO. Centralised FSSAI-certified processing facilities handle cutting, marination, packaging, and quality testing. Refrigerated cold-chain logistics deliver to consumers within thirty to ninety minutes depending on micro-market order density, according to publicly reported operational parameters. The company disclosed that approximately 80 to 85 percent of revenue is generated through its owned app, a metric it has cited as evidence of direct consumer relationships and reduced platform dependency.

Licious has structured its product portfolio across several sub-categories. These include raw fresh meat and seafood in standardised cuts, marinated ready-to-cook products, cold cuts and deli items, and ready-to-eat offerings. The ready-to-cook and value-added segments carry higher average realisations than raw commodities, and their expansion represents a deliberate premiumisation and margin improvement strategy. The company has also separately launched a plant-based sub-brand called Uncrave, targeting flexitarian consumers — a small contributor to current revenue but strategically significant as a brand extension and ESG narrative for institutional investors at IPO stage.

The subscription programme, branded Infiniti, has publicly disclosed 1.5 lakh active subscribers who contribute approximately 40 percent of the company's monthly business. The company has set a target of 250,000 active subscribers within the same fiscal year this figure was reported. The average order value stands at approximately ₹600, up from ₹500 three to four years prior, reflecting category premiumisation and the growing share of value-added products in the basket.

Positioning & Consumer Insight

The central consumer insight that Licious has built its brand positioning around is the separation of meat consumption from the purchasing experience. In traditional wet markets, the act of buying meat was inseparable from its environment — unrefrigerated display, uncertain provenance, unhygienic handling, and inconsistent quality. This created a class of aspirational meat consumers, primarily urban and upper-middle income, who were willing to spend more but had no credible premium channel through which to do so.

Licious positioned itself as the resolution to this gap by making freshness a guaranteed and verifiable product attribute rather than an ambient claim. The brand's communication consistently emphasised FSSAI certification, cold-chain traceability, antibiotic-residue testing, and absence of artificial preservatives. The brand coined the term "Licious Standard" to describe this quality benchmark — a positioning device that functions as a category claim as much as a brand claim, asserting that the relevant comparison for a Licious product is not a competing branded player but the traditional wet market alternative.

This positioning was reinforced through packaging that deliberately communicated the absence of intervention — no preservatives, no prior freezing, no artificial colouring — and through the delivery proposition of sub-ninety-minute freshness windows that structurally prevented inventory ageing from becoming a quality risk. In effect, the brand's operational model and its positioning were the same argument expressed in two different languages.

Media & Channel Strategy

No verified public information is available on Licious' specific above-the-line advertising spend, agency relationships, or detailed media allocation across fiscal years.

What is publicly documented is the company's channel architecture. Licious has operated with approximately 80 to 85 percent of its revenue generated through its owned mobile application. The company has engaged quick commerce platforms as an incremental distribution channel, with quick commerce deliveries growing 35 percent year-on-year in FY24 even as total revenue contracted. The company has been piloting thirty-minute delivery capability in Gurugram, representing a direct competitive response to the speed proposition of quick commerce players.

On offline expansion, Licious disclosed plans to open 500 stores in twenty Indian cities over five years, with concentration in eight major metros. The company has approximately $100 million allocated for this expansion. In a notable early execution of this strategy, Licious acquired Bengaluru-based offline meat retailer My Chicken and More, which operated 23 stores across the city, in October 2024. The strategic rationale disclosed was to attract new users through offline discovery and convert them into online transactors, combining the acquisition efficiency of physical retail with the margin and loyalty mechanics of owned digital channels.

Business & Brand Outcomes

Licious' financial trajectory reflects the structural tension between premium positioning and the economics of perishable goods delivery in a price-sensitive market.

Revenue grew from ₹682.5 crore in FY22 to ₹746 crore in FY23. In FY24, revenue declined 8.4 percent to ₹685 crore, a contraction the company attributed to the closure of the Dunzo platform and Swiggy Meatstore as distribution channels, and to a deliberate wind-down of modern trade and general store exposure. The company was explicit that platform-driven sales on its own app grew 5 percent during the same period, suggesting the revenue decline was a managed strategic consequence rather than a demand-side failure. In FY25, revenue recovered to ₹797 crore, representing 16 percent year-on-year growth from FY24.

On profitability, net losses have declined steadily in recent years. From a loss of ₹528.5 crore in FY23, losses contracted 44 percent to ₹293.77 crore in FY24. In FY25, losses narrowed a further 27 percent to ₹218.3 crore. Total expenses in FY25 rose only 1.4 percent year-on-year despite 16 percent revenue growth, indicating meaningful operating leverage being unlocked through the channel and cost restructuring of FY24.

The company processes over 1.2 million orders monthly and serves a base of four million households. The Infiniti subscription programme accounts for 40 percent of monthly business at 1.5 lakh active subscribers, with a publicly stated expansion target of 250,000 subscribers.

Licious achieved unicorn status in October 2021 with a valuation exceeding $1 billion, and its last formally reported valuation as of September 2023 stood at ₹12,100 crore (approximately $1.47 billion). The company has publicly stated plans for a pre-IPO funding round in 2026 and an IPO targeting a valuation in excess of $2 billion.

Strategic Implications

Several analytically significant strategic themes emerge from the Licious case.

Infrastructure as Brand: The most transferable lesson from Licious is the inversion of conventional brand logic. In most consumer businesses, brand identity is constructed through communication and then delivered through operations. In Licious' case, the operational architecture — cold chains, certified processing, traceability systems — is the brand's fundamental credibility claim. Communication follows infrastructure rather than preceding it. This has profound implications for brands attempting to enter any category where consumer trust is the primary purchase barrier.

The Premiumisation Ceiling in Perishables: Licious has demonstrated that premiumisation in perishable foods is achievable in Indian urban markets but is constrained by the cost structure of its own differentiation. The cold-chain infrastructure, quality testing, and thirty-to-ninety-minute delivery economics are simultaneously what enable the premium claim and what prevent easy margin expansion. This tension — where the product's core value proposition is also its primary cost driver — is the central unit economics challenge the company must resolve before public market listing.

Channel Strategy as Brand Strategy: The decision to grow through an owned app rather than platform dependency, and to invest in offline retail to serve as a customer acquisition funnel into digital channels, reflects a brand view of channel architecture. Each channel choice is evaluated not only for revenue but for the type of consumer relationship it enables. The Dunzo and Swiggy Meatstore exits, despite short-term revenue impact, reflect a strategic preference for owned consumer relationships over volume transacted through third-party platforms.

Quick Commerce as Structural Disruption: The entry of Zepto's Relish brand into the meat category, reportedly generating ₹150 crore in annualised recurring revenue within six months of launch, represents a category-level disruption that Licious' vertical integration model was not originally designed to absorb. Licious' response — investing in thirty-minute delivery capability and expanding its quick commerce presence while maintaining own-app primacy — suggests a hybrid defensive posture that will require continued capital and operational agility to sustain.

IPO Readiness and the Profitability Imperative: Licious has raised approximately $490 million over a decade without achieving profitability in any reported fiscal year. The sustained narrowing of losses in FY24 and FY25, combined with the articulated EBITDA breakeven target and offline expansion funded through existing balance sheet, suggests that the company's strategic decision-making from this point is substantially shaped by public market readiness rather than growth maximisation alone. This is a meaningful shift in strategic orientation for a company that spent its first seven years building category infrastructure.

Discussion Questions for MBA

1. Licious built its brand positioning almost entirely on supply chain capability rather than conventional marketing. Under what market conditions is this approach replicable, and what are the risks when a competitor can match or exceed that infrastructure investment?

2. The company deliberately reduced revenue in FY24 by exiting third-party distribution channels to improve unit economics and strengthen direct consumer relationships. Evaluate this trade-off from a brand equity and investor relations perspective. Was this the right decision at this stage of the company's lifecycle?

3. Licious is expanding offline through acquisitions and company-owned stores while simultaneously deepening its quick commerce presence. How should the company prioritise these channels to avoid brand dilution and operational overextension as it approaches an IPO?

4. Zepto's Relish entered the branded meat category and reportedly scaled to significant revenue within months by leveraging existing quick commerce infrastructure and no cold-chain capital expenditure of its own. How should Licious reframe its vertical integration advantage in a competitive environment where speed-to-market without infrastructure is increasingly possible?

5. Licious has never reported a profitable fiscal year despite raising approximately $490 million over ten years. At what point does sustained unprofitability become a brand liability with consumers, and how should the company communicate its path to profitability without undermining the quality and premium associations it has spent a decade building?

Comments